Okta shares spiraled lower following a disappointment in the company’s outlook despite reporting solid second-quarter results. Investor sentiments took a hit despite Okta’s Q2 revenue jumping 16%, and subscription revenue climbing 17% year over year. Adjusted earnings per share also surged from $0.31 to $0.72.

A Bumpy Ride: Solid Quarter, Weak Outlook

Despite a 16% rise in remaining performance obligation (RPO) backlog and a 13% increase in current RPO (cRPO) backlog, based on signed contracts as indicators of future revenue, Okta’s net dollar retention rate remained steady at 110%. The company now stands at 19,300 customers, with a growing number of high-value contracts.

While Okta has raised its guidance for fiscal 2025, the conservative approach in light of past security incidents and macro uncertainties has left investors craving for more. The company’s growth potential is questioned, despite its efforts to strengthen its enterprise foothold.

Assessing the Dip: Time to Buy?

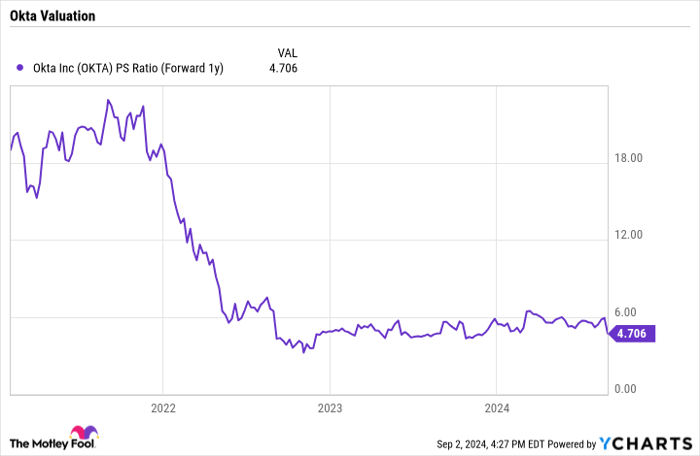

With Okta’s current valuation at a forward price-to-sales ratio of less than 5, the stock is trading at a significant discount compared to its peers in the cybersecurity industry. The market reaction seems exaggerated, considering Okta’s consistent performance and cautious guidance strategy.

Image source: Getty Images.

Investor concerns have been lingering regarding competitive threats and past security breaches impacting Okta’s growth trajectory. Despite these challenges, the current valuation could present a buying opportunity for those betting on Okta’s long-term potential.

Deciding on Investing in Okta

Before making a decision to invest in Okta, it’s crucial to weigh the risks against the potential rewards. While top analysts may not have named Okta among the top stocks to watch, the stock’s undervaluation could hint at untapped growth opportunities.

OKTA PS Ratio (Forward 1y) data by YCharts

Reflecting on historical cases like Nvidia’s meteoric rise post-recommendation, it’s evident that overlooked stocks can yield massive returns when given due consideration. The cautious stance taken by Okta’s management may dampen immediate optimism, but also presents a chance for savvy investors seeking discounted growth opportunities.

Disclaimer: The author has no position in any stocks mentioned. Please perform due diligence before investing.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.