Canadian Pacific Kansas City’s CP operations stand tall amidst a railway landscape that demands more than just keeping pace. Unwavering in its quest for operational excellence, CP’s efficiency drive and cost-saving maneuvers anchor its performance, standing as a beacon for stakeholders. Yet, lurking in the shadows are the formidable foes of soaring fuel costs and a liquidity quagmire that threaten to cast a pall over the company’s otherwise stellar trajectory.

Factors Driving CP’s Success

Canadian Pacific orchestrates a symphony of efficiency, exemplified in its stellar second-quarter showings. A 9% dip in average terminal dwell signifies the gears of processing and handling running smoother. The network breathes as train speeds quickened by 6%. Locomotive productivity and fuel efficiency stretched by 10% and 2% respectively, echoing CP’s unwavering commitment to operational brilliance and sustainability.

Moreover, the company’s surgical precision in slashing costs is paying dividends. Labor outlays, constituting 26.2% of total operating expenses, dipped by 7% to $612 million year over year in Q2 of 2024.

Not forgetting its shareholders, CP has woven a tapestry of confidence through consistent dividends. The company’s dividend journey from C$507 million in 2021 to C$707 million in 2022 and 2023 attests to its financial prowess and proactive stance in rewarding its faithful. In Q2 of 2024, a quarterly dividend of 19 cents per share was the sweet melody played for shareholders’ ears.

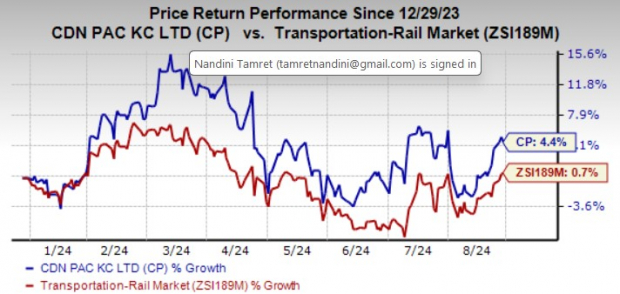

The stock of Canadian Pacific has forged ahead, posting a 4.4% rally year to date, overshadowing the industry’s paltry 0.7% growth in the corresponding period.

Challenges on CP’s Horizon

However, the harsh winds of high fuel costs loom ominously. In Q2 of 2024, these costs surged by a worrisome 17% compared to the previous year.

At the tail end of June’s quarter, Canadian Pacific found itself clenching $557 million in cash and cash equivalents while bearing the weight of a current debt load of $3.67 billion. The glaring gap indicates a liquidity tightrope walk—cash falling short to meet pressing financial needs.

With a current ratio of 0.51 at the close of Q2 in 2024, CP’s liquidity measure raises a caution flag – a ratio below 1 spelling out challenges to meet immediate obligations.

CP’s Zacks Rank

Presently, Canadian Pacific carries a Zacks Rank #3 (Hold).

Stocks Worth Deliberation

For investors with itchy trigger fingers, potential gems in the Zacks Transportation sector like C.H. Robinson Worldwide and Westinghouse Air Brake Technologies offer enticing prospects.

C.H. Robinson Worldwide flashes a Zacks Rank #1 (Strong Buy). Not to be overlooked is the juicy expected earnings growth rate of 25.2% for the current year.

The company’s knack for surprises is evident in its earnings history. Outshining the Zacks Consensus Estimate in three out of the last four quarters, with an occasional miss, pins an average surprise of 7.3%. CHRW shares have been basking in the sun, up 9.9% over the past year.

WAB dons a Zacks Rank #2 (Buy) currently and anticipates an earnings growth rate of 26% for the current year.

In the earnings surprise hall of fame, Westinghouse Air Brake Technologies shines bright, having outperformed the Zacks Consensus Estimate in all of the trailing four quarters, boasting an average beat of 11.8%. The allure of WAB shares is apparent, having surged by 46.2% over the prior year.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.