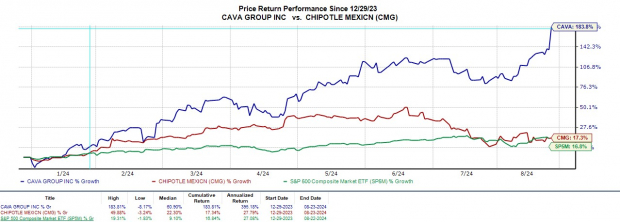

Comparing to a Chipotle Mexican Grill in Mediterranean cuisine, Cava Group has been a stellar performer since its IPO last year.

Cava Group’s stock surged after surpassing Q2 top and bottom line expectations.

Cava Group posted Q2 sales of $233.5 million, up 35%, and beat estimates by 5%. The bottom line saw a dip but still exceeded expectations. Traffic spiked by 9.5%, and 18 new restaurants were opened to enter the Midwest market.

Cava Group is on a growth trajectory, with estimated sales to climb 24% in fiscal 2024 to $907.58 million. Annual earnings are expected to soar 66% to $0.35 per share versus last year.

Despite the growth, Cava Group is trading at a forward earnings premium of 291.3X and a noticeable sales premium to the broader market at 12.8X.

Cava Group’s monstrous YTD rally has led to a stretched valuation, reflected in its Zacks Rank #3 (Hold). It remains an intriguing long-term investment with potential buying opportunities.

Exploring Investment Potential

Is now the time to invest in Cava Group’s promising expansion or wait for a dip in stock prices?

History of Earnings Exceeding Expectations

Having consistently outperformed in earnings over the past five quarters, will Cava Group continue its impressive track record?

Evaluating Market Comparisons

Comparing Cava Group’s valuation to industry peers and broader market averages, is the current premium justified?

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.