Snowflake shares plummeted over 12% post the fiscal second-quarter 2025 results, leaving investors reeling from the sudden chill. Despite boasting sturdy adoption rates of its solutions, Snowflake’s product revenues soared by a meager 29.5% year over year to $829.3 million.

For fiscal 2025, SNOW envisages a 26% uptick in product revenues, raking in $3.36 billion, which, though better than previous projections, indicates a sluggish growth pace compared to the robust 38% witnessed in fiscal year 2024.

Although retaining its non-GAAP product gross margin at 75%, SNOW expects a contraction in gross and operating margins by 300 and 500 basis points, respectively. Moreover, the outlook for a 26% non-GAAP adjusted free cash flow margin in fiscal 2025, down from 29% in 2024, paints a worrisome picture.

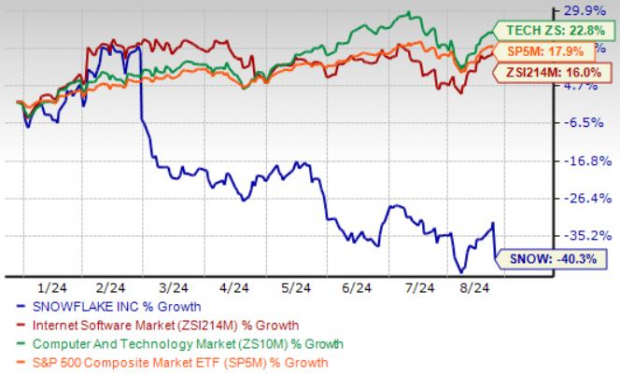

The descent in SNOW’s share price can be largely attributed to a bleak margin forecast, primarily due to escalating GPU costs. Year to date, SNOW shares have nosedived by 32.1%, significantly lagging behind the Computer & Technology sector’s return of 22.8%.

Year-to-Date (YTD) Performance

While celebrations may have been premature, the aftermath reveals a sobering truth – Snowflake’s performance has been on a slippery slope, much to the dismay of market spectators.

Snowflake Snowed under Mounting Expectations

The aftermath of the fiscal second quarter tells a tale of Snowflake’s earnings, which at 18 cents per share failed to keep warm investor sentiment, flagging an 18.2% decline year over year. Revenues of $868.8 million managed to scrape past expectations by 2.26%, showcasing a 29% year-over-year climb.

As the numbers unfolded, Snowflake found itself grappling with a net revenue retention rate of 127% for existing customers, a mere speck in the storm of challenges ahead.

Amidst the turmoil, the count of customers at 10,249 recorded a 21.2% uptick year over year, with a fraction boasting trailing 12-month product revenues exceeding $1 million.

Forecasting the Snowstorm: Third Quarter Projections

Peering into the crystal ball for the third quarter, Snowflake anticipates product revenues ranging between $850-$855 million, hinting at a 22% year-over-year expansion. However, dark clouds gather as the Zacks Consensus Estimate foresees a 40% year-over-year earnings decline.

Snowflake Stock: A Melting Pot of Concerns

Despite appearances, the Snowflake stock glimmers with uncertainty, portraying a value score of F in terms of valuation. Trading at a significant premium compared to the sector, SNOW’s future seems clouded with ambiguity, as reflected by its downward trajectory below the 50-day moving average.

Unveiling the Core: Snowflake’s Expanding Universe

As Snowflake charts new territories, its recent introductions like Marketplace Listing Auto-Fulfillment & Monetization, Query Acceleration Service, and geospatial analytics, in a flurry of activity, might signal a fresh dawn amid the chaos.

By launching Polaris Catalog, Snowflake offers a lifeline to enterprises seeking stability in turbulent times. With support from industry giants like Amazon’s AWS, Microsoft Azure, Salesforce, and more, Snowflake’s expanding partner network could hold the key to weathering the storm.

Epilogue: A Silver Lining or a False Dawn?

As the dust settles on Snowflake’s rocky quarter, a cautious optimism prevails. With a Zacks Rank of 3 (Hold), awaiting a more opportune moment to venture into SNOW remains the wisest course amidst the tumultuous market winds.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.