Following a recent market slump, numerous companies emerge as enticing bargains. The transient headlines fueling this downturn will hold little sway in the grand timeline of three to five years—there’s no need for undue alarm.

Standing out prominently on the current shopping roster are Taiwan Semiconductor Manufacturing, Alphabet, and Amazon. These three industry giants boast robust long-term growth factors, presenting themselves as compelling investment opportunities in the present climate.

Emblem of the Semiconductor Industry: Taiwan Semiconductor

Regarded by many as the linchpin of the technology sector, Taiwan Semi plays a pivotal role in the intricate web of high-tech innovation. Its cutting-edge semiconductor manufacturing prowess under the 3nm umbrella places it in a league of its own, indispensable to tech giants like Apple and Nvidia.

Deploying sophisticated production methodologies demanding immense expertise, TSMC enjoys a near-insurmountable position in the industry, despite facing formidable rivals. With its stock presently trading at a 10% discount from 2024 peaks, the investment remains attractive, even for those who may have missed the precise bottom.

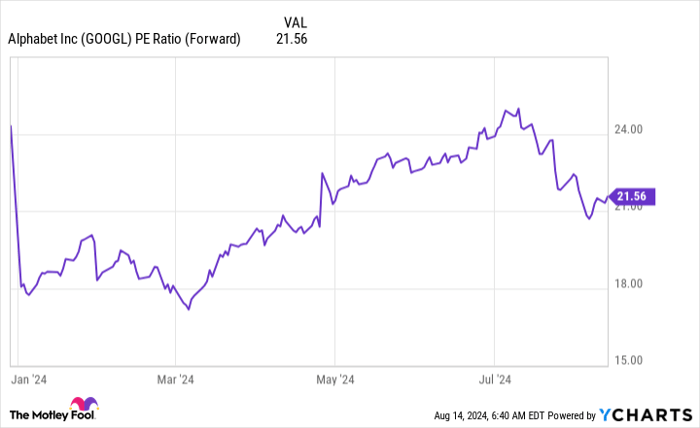

Alphabet: Unraveling the Value Amidst Tech Titans

Even before the market slip, Alphabet stood out as a prime asset beckoning investors. Despite flaunting a dominant position as one of the world’s largest corporations, Alphabet’s valuation doesn’t carry the premium often associated with its tech counterparts. With a mere 22 times earnings price tag, Google’s parent entity emerges as one of the more reasonably priced big tech stocks.

Amazon: Navigating the Earnings Landscape

Amazon might appear to be the laggard among the trio in investors’ eyes. In Q2, the tech behemoth saw sales growing by a “modest” 10% to $148 billion, slightly underwhelming market expectations. Additionally, its Q3 revenue forecast of 8% to 11% failed to impress the crowds.

However, fixating on these figures might miss the point. The real story lies in Amazon’s burgeoning profitability trajectory, with operating income poised to surge between $11.5 billion and $15 billion in the forthcoming quarter—a substantial uptick from the year-ago period.

The Long Game in Investment: Understanding Amazon’s Trajectory

While Amazon’s forward P/E ratio of 36 may not scream “cheap,” the focus on maximizing profitability is paramount. Amazon’s strategy entails accelerating earnings growth at a faster pace than its revenue, an endeavor that requires time to materialize. Investors willing to look beyond immediate revenue growth concerns may find Amazon’s lowered stock price an opportune entry point.

Exploring Investment Prospects in Taiwan Semiconductor Manufacturing

Before delving into Taiwan Semiconductor Manufacturing stocks, it’s essential to weigh the following aspects:

The Motley Fool Stock Advisor team recently outlined their coveted list of the top 10 stocks to watch, with Taiwan Semiconductor Manufacturing missing the cut. The historical precedent, exemplified by Nvidia’s stellar growth, demonstrates the prodigious gains long-term investments can reap.

Stock Advisor not only furnishes investors with a strategic blueprint for success but also exemplifies a track record that has handily outperformed the S&P 500 since 2002.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.