The 2024 Q2 earnings season is gradually drawing to a close, exuding a positive and promising vibe. Earnings growth has remained buoyant, with a trajectory set to stay positive in the upcoming Q3 cycle.

This week, Walmart (WMT) and Alibaba (BABA) are set to unveil their quarterly financial results. Both firms have stamped their authority in the eCommerce domain, with Walmart still fine-tuning its digital engagement strategies.

These reports will offer a deeper insight into the current consumer landscape. Let’s delve into the comparative analysis of each company’s performance.

Walmart’s Profit Uplift

The retail juggernaut Walmart, currently seated at Zacks Rank #2 (Buy), has reaped the rewards of its digital forays, significantly boosting its quarterly figures in recent times. Year-to-date, its shares have surged by over 30%.

The latest quarterly results have fueled an uptick in shares, as depicted below.

Image Source: Zacks Investment Research

Global eCommerce sales recorded a robust 21% year-over-year growth in the most recent period, elucidating yet another stellar quarter for the company in this metric. Moreover, eCommerce penetration witnessed an uptick across all Walmart markets in the same period.

The focus will likely remain on this metric in the forthcoming earnings release, as favorable outcomes would further cement its eCommerce momentum. It’s essential to note that the company’s eCommerce sales encompass store pickups as well.

The company’s profitability has seen a notable upswing in recent times due to cost efficiencies, leading to margin expansion, as illustrated below. It’s crucial to bear in mind that the chart is based on a trailing twelve-month period.

Image Source: Zacks Investment Research

Walmart’s quarterly disclosure stands as one of the most pivotal in the overall retail landscape. The company’s value proposition positions it favorably to attract consistent demand from budget-conscious consumers, with affluent consumers also gravitating toward Walmart during economic downturns. The surge in market share in its U.S. outlets in the recent period was predominantly steered by higher-income households.

It’s worth highlighting that valuation multiples are elevated as we approach the release, with the current forward 12-month earnings multiple standing at 26.6X, well above the 23.3X five-year median. The stock holds a Value Style Score of ‘C.’

Image Source: Zacks Investment Research

Earnings and revenue projections have remained stable over recent months, with Walmart expected to post 6.5% growth in earnings on 4% higher sales.

Alibaba’s Cloud Endeavors Under Scrutiny

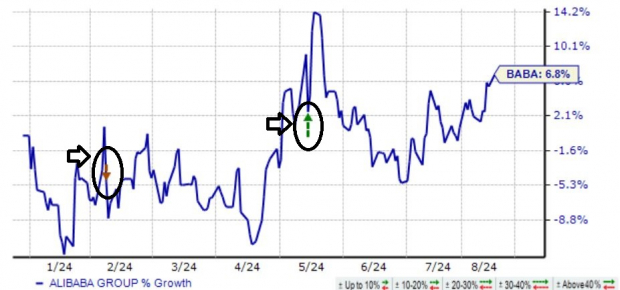

Alibaba’s share performance in 2024 has been a rollercoaster ride, witnessing an overall ascent of nearly 7% and experiencing mixed reactions post-earnings. From a long-term perspective, the stock has been somewhat challenging to hold, on a 55% decline over the past three years, with its China exposure adding to the regular volatility.

Image Source: Zacks Investment Research

An area of keen interest in the upcoming release will be the additional insights provided on its cloud and AI initiatives. Alibaba enjoyed a fruitful period concerning its endeavors in the cloud sphere in its latest report, asserting, ‘During the quarter, our core public cloud offerings, which comprise products like elastic compute, database, and AI products, witnessed double-digit year-over-year growth in revenue.’

Despite Alibaba’s dent in cash-generating capabilities, it is vital to recognize that the dip is attributed to escalated capital expenditures directed at fortifying its cloud infrastructure. Free cash flow saw a 50% decline year-over-year in the recent period. Positivity surrounding its cloud investments could potentially trigger a favorable post-earnings trajectory.

The stock currently sits at Zacks Rank #4 (Sell), with analyst sentiment for the upcoming release skewing towards pessimism.

Image Source: Zacks Investment Research

Final Verdict

As we brace for a flurry of company announcements this week, the spotlight remains on Walmart (WMT) and Alibaba (BABA).

Investors tracking Walmart should home in on its eCommerce metrics, which have been a powerful ally for the company in recent quarters, bolstered by robust growth. Walmart finds itself in a ‘sweet spot,’ catering consistently to budget-conscious consumers while also capturing the attention of upscale consumers during economic squeezes.

For Alibaba, the focus will likely center on its cloud and AI strategies, characterized by heavy capital injections. Keep an eye on the Gross Merchandise Volume (GMV), providing insights into the current consumer sentiment.

With Alibaba sporting a less favorable Zacks Rank #4 (Sell) compared to Walmart’s Zacks Rank #2 (Buy), Walmart shares appear more enticing than Alibaba’s in the lead-up to the disclosure.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.