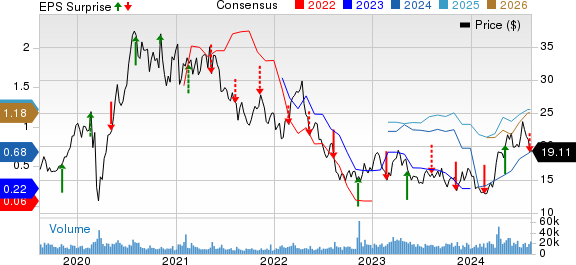

Pan American Silver Corp. PAAS fell short of expectations in the second quarter of 2024, reporting adjusted earnings per share of 11 cents, missing the Zacks Consensus Estimate of 15 cents. Despite this setback, the company recorded an improvement from the year-ago quarter, with adjusted earnings per share rising from 8 cents to 11 cents.

With revenues showing a commendable 7.3% year-over-year growth to $686 million, PAAS managed to surpass the Zacks Consensus Estimate. Notably, the average realized silver price increased by 20% to $28.14 per ounce, while the average realized gold price saw a substantial 18.3% year-over-year surge to $2,336 per ounce.

Pan American Silver Corp. Price, Consensus and EPS Surprise

Pan American Silver Corp. price-consensus-eps-surprise-chart | Pan American Silver Corp. Quote

Operational Performance

Despite challenges, PAAS saw a decline in silver production by 24.2%, amounting to 4.57 million ounces in the quarter. Conversely, gold production witnessed a year-over-year drop of 11.2%, totaling 220.4 thousand ounces in the reported period.

The increase in cash costs for both the Silver and Gold segments paints a challenging picture for the company. The Silver segment witnessed a 56% rise in cash costs, while the Gold segment saw a 13.5% increase. Additionally, all-in sustaining costs (AISC) for both segments climbed, with the Silver segment up by 21.5% and the Gold segment up by 18%.

Despite these hurdles, PAAS reported mine-operating earnings of $117 million in the quarter, showing resilience in a tough market.

Financial Stability

As of the end of the second quarter of 2024, Pan American Silver had a healthy financial position, with $368.6 million in cash and short-term investments. The company also has $750 million available in its revolving credit facility. However, total debt amounted to $809.5 million.

PAAS reported a significant increase in net cash generated from operations, signaling operational efficiency and financial discipline. The company generated $163 million in net cash from operations in the second quarter, compared to $117 million in the same period last year.

Looking Ahead: Guidance and Expectations

PAAS reaffirmed its production guidance for 2024, with silver production expected to range between 21 million and 23 million ounces. Gold production is estimated to fall between 880,000 ounces and 1,000,000 ounces. The company also provided AISC guidance, reflecting its commitment to cost management and operational excellence.

Price Performance and Industry Comparison

Despite the challenges faced, PAAS shares have demonstrated resilience, gaining 24.2% in the past year. Although slightly underperforming the industry, this growth showcases the company’s ability to navigate uncertain market conditions.

Image Source: Zacks Investment Research

Peer Analysis

Comparatively, PAAS’ peers in the industry have faced a mixed bag of results. While Hecla Mining showed improvement in earnings and silver production, Buenaventura Mining struggled with a shortfall in earnings despite a significant revenue increase.

Anticipating Future Performance

As the industry awaits the second-quarter results from Avino Silver ASM, investors are keen on the company’s performance. With a history of negative surprises, the company is expected to unveil its financial standing and operational outlook on August 13.

With the second quarter showing a promising yet challenging outlook for PAAS and its peers, the dynamics of the precious metals industry continue to evolve, presenting both risks and opportunities for investors seeking exposure in this sector.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.