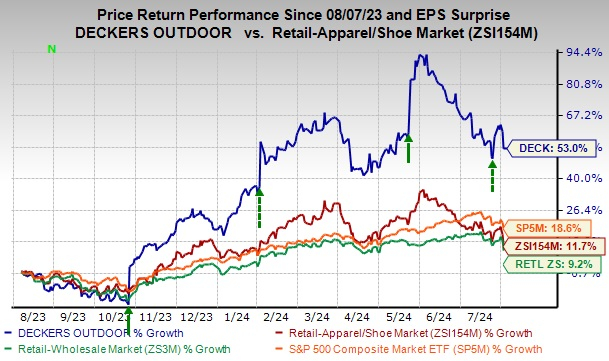

Deckers Outdoor Corporation DECK has seen a meteoric rise in its stock price over the past year. Surging by a staggering 53%, the company has left its mark in the Zacks Retail-Apparel and Shoes industry, outpacing the industry’s meager 11.7% growth. Through a steadfast focus on expanding their brand presence and fortifying direct-to-consumer (DTC) channels, Deckers has managed to navigate the turbulent waters of the market with finesse.

Refusing to be a mere bystander, Deckers’ strategic prowess has propelled it to outperform the broader Retail-Wholesale sector and the S&P 500 index, which saw growth rates of 9.2% and 18.6% respectively during the same period.

As technical indicators paint a picture of triumph, Deckers’ stock confidently hovers above both its 100-day and 200-day moving averages. This firm positioning signals unwavering upward momentum and price stability, a testament to the market’s robust belief in Deckers’ financial vitality and long-term promise. Garnering an A on the Value Score scale, Deckers stands as a paragon of appeal in the current market scenario.

Image Source: Zacks Investment Research

Unpacking the Favorable Winds

Riding the waves of prosperity, Deckers has steered towards lucrative markets, fostered product innovation, expanded its physical footprint, and amplified e-commerce capabilities. This concerted effort has elevated the popularity of UGG and HOKA brands and fortified its international outreach. With aspirations of propelling HOKA into a multibillion-dollar entity, establishing UGG as a global lifestyle emblem, and fortifying its DTC arm, Deckers is setting sail on a journey towards unrivaled success.

Deckers’ robust DTC business and omnichannel expansion strategy have borne fruit, with DTC net sales swelling by 24% in the initial quarter of fiscal 2025. The company’s alignment of product creation, marketing strategies, and distribution channels according to consumer demands has been a harbinger of substantial growth. Strategic moves like opening new stores and targeted market expansions have not only enhanced brand accessibility but have also enriched consumer experiences.

At the cornerstone lies product innovation, a cornerstone of Deckers’ strategy, reflected in the triumphant unveiling of new styles and collections. By engaging consumers through brand activations, collaborations, and social listening initiatives, Deckers has forged lasting brand loyalty. The advent of products such as the Cielo X1 and Skyward X underscores Deckers’ unwavering commitment to performance and technological progression.

While the wholesale channel remains an indispensable cog in the wheel, Deckers witnessed a 21% year-over-year surge in first-quarter revenues, with a strong foothold in the United States and Europe. The company’s international stride has proven to be particularly effective, as international sales swelled by 20.8% year over year, fueled by robust DTC growth and well-thought-out wholesale alliances, especially in the Chinese and EMEA markets. This strategic stance has solidified Deckers’ stature as a global titan in the footwear realm.

Embracing Shareholder-Friendly Ventures for a Rosy Outlook

Deckers isn’t merely basking in its glory but is fortified by a robust liquidity cushion, courtesy of a formidable cash reserve. As of June 30, 2024, Deckers boasted a sizable $1.44 billion in cash and cash equivalents, augmenting its financial dexterity. Notably, Deckers stood tall without any outstanding debts during this period, embodying a healthy financial profile. The company reported a net cash flow of $112.7 million from operating activities as of June 30, 2024.

In the initial quarter, DECK exhibited its unwavering trust in its financial prowess by repurchasing roughly 177,000 shares amounting to $152 million. This bold move not only underscores management’s dedication to enhancing shareholder value but also underscores their unwavering faith in the company’s future prospects. As of June 30, 2024, DECK had $789.7 million still up for grabs under its share repurchase authorization.

The Road Ahead for Growth

Setting its sights high, Deckers forecasts a 10% surge in fiscal 2025 net sales, reaching a notable $4.7 billion milestone. Projections indicate a 20% growth trajectory for HOKA, fueled by consumer gains in the DTC channel, expansive strategic partnerships, and international market upsurge. Meanwhile, UGG is slated for a mid-single-digit escalation, propelled by international expansion and a robust U.S. market. Anticipated earnings for fiscal 2025 hover in the range of $29.75-$30.65 per share, marking a promising climb from last year’s $29.16.

Reshaping Estimates in Favor of the Stock

The Zacks Consensus Estimate for earnings per share has witnessed an upward wave, reflecting the prevailing positive sentiments surrounding Deckers. Over the previous 30 days, analysts have hiked up their estimates for the current and next fiscal year by 3% to $31.52 and 2.4% to $35.18 per share, hinting at year-over-year growth rates of 8.1% and 11.6%.

Concluding Remarks

Despite an optimistic outlook, Deckers remains wary of gross margin pressures stemming from escalated freight costs and a return to a more conventional promotional setting. However, astute investors would be remiss to overlook Deckers as an investment avenue given its robust financial health and liquidity underscored by a solid cash reserve and absence of any looming debts.

The company’s stellar performance across both DTC and wholesale segments is a testament to its operational dexterity and expansive market foothold. Moreover, the prevailing positive market sentiment and upward revisions in earnings forecasts substantiate the unwavering faith in Deckers’ ongoing triumph and growth prospects. Standing tall with a Zacks Rank #2 (Buy), Deckers beckons discerning investors towards a promising horizon.

Exploring Other Gemstones in the Retail Realm

Casting a glance across the retail expanse, some noteworthy stocks worth pondering include The Gap, Inc. GPS, Abercrombie & Fitch Co. ANF, and Urban Outfitters Inc. URBN.

Gap, an illustrious international specialty retailer offering a diverse array of clothing, accessories, and personal care products, currently gleams with a Zacks Rank #1 (Strong Buy).

Forecast trends for Gap’s fiscal 2024 earnings and sales signal a surge of 24.5% and 0.2% respectively from the fiscal 2023 figures. Noteworthy is Gap’s trailing four-quarter average earnings surprise, standing tall at a remarkable 202.7%.

Abercrombie, a connoisseur in premium, high-quality casual apparel, presents itself with a Zacks Rank of 1. ANF recently delivered a staggering 28.9% earnings surprise in its latest reported quarter.

Projections for Abercrombie’s fiscal 2024 earnings and sales point towards a growth of 48.9% and 11.1% respectively from the fiscal 2023 reported benchmarks. Not to be overlooked is Abercrombie’s impressive trailing four-quarter average earnings surprise, pegged at an astounding 210.3%.

Urban Outfitters, a beacon in the lifestyle specialty retail world, promising an array of fashion apparel, accessories, footwear, home décor, and gift items, currently showcases a Zacks Rank of 2.

Forecasts hint at Urban Outfitters’ fiscal 2024 earnings and sales scaling up by 9.9% and 5.8% respectively from the actual figures of yesteryears. Urban Outfitters has been consistently delivering an average earnings surprise of 16.9% over the past four quarters.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.