Few things in life compare to the frustration of witnessing a rival outshine you as you struggle to keep pace. The story of Ford Motor Company (NYSE: F) during its recent second-quarter earnings announcement perfectly encapsulates this sentiment. With a 35% earnings dip to $0.47 per share, driven by surging warranty costs and losses in its electric vehicle (EV) segment, Ford found itself in an unenviable position. Meanwhile, crosstown competitor General Motors exceeded expectations and even raised its full-year earnings forecast. The aftermath for Ford was brutal, experiencing its worst trading day since 2008. Yet, amidst the chaos, there are glimmers of hope that may buoy long-term investors.

Revitalized Quality Standards

Recent years have seen Ford’s esteemed reputation for vehicle quality take a significant hit. While recalls are par for the course in the automotive industry, the magnitude of Ford’s recalls, particularly on older models from 2016 to 2021, has dealt a severe blow to its financial performance. However, under the stewardship of CEO Jim Farley, quality improvement has emerged as a top priority. Notable progress was evidenced in J.D. Power’s 2024 U.S. Initial Quality Study, where Ford surged 14 spots to claim the ninth position. While the benefits of these newer quality standards will only be fully realized in the next 12 to 18 months, management anticipates a return to expected results in the latter part of 2024.

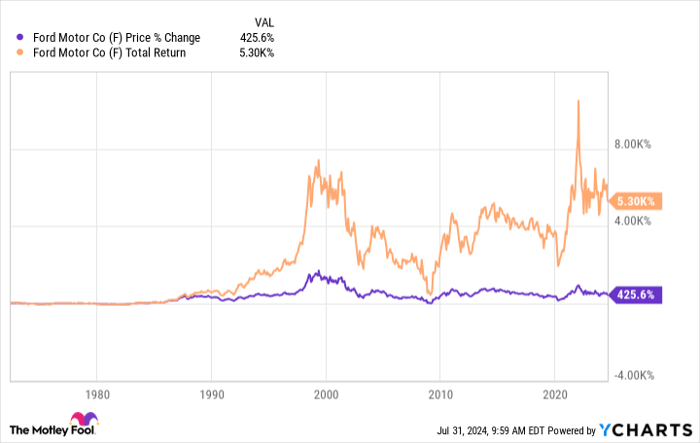

The Dividend Advantage

In the realm of portfolio returns, dividends wield considerable influence, especially when reinvested. A case in point is Ford, whose total returns, inclusive of dividends, overshadow mere stock price gains.

Ford’s quarterly dividend of $0.15 per share boasts a noteworthy 5.5% yield. Notably, Ford has committed to allocating 40% to 50% of its free cash flow to investors primarily through dividends, eschewing share repurchases as a primary means of capital return. Such commitment often paves the way for special dividends, such as the additional $0.18 per share following the 2023 fourth quarter, and a substantial $0.65 per share special dividend post the 2022 fourth quarter.

Driving Profits with Ford Pro

Central to Ford’s financial success is its Ford Pro division, a segment dedicated to commercial operations, encompassing vans, Super Duty trucks, and fleet subscription services.

During the first half of 2024, Ford Pro delivered a 21% revenue upsurge, clocking in a robust $5.6 billion in EBIT and enjoying a 16% EBIT margin. In stark contrast, Ford Blue, the legacy internal combustion engine vehicle business, witnessed a 3% revenue decline, generating a meager $2 billion in EBIT, boasting a paltry 4.3% EBIT margin. Subscriptions to Ford Pro software spiked by 35% in Q2, with mobile repair orders doubling. Particularly lucrative, the Ford Pro division holds promise as Ford rejigs its strategy at the Ontario, Canada-based Oakville plant, focusing on an additional 100,000 Super Duty trucks production over two new electric vehicles originally planned. This tactical adjustment will undoubtedly bolster short-term results amidst supply constraints.

The Road Ahead

Undeniably, Ford faces a barrage of challenges in the near future – from revamping quality standards to curbing warranty costs and reversing EV losses. However, the company stands to gain significantly by achieving breakeven in its EV operations over the coming years, sustaining its dividend policy, and expanding subscription services and sales through Ford Pro. These factors underscore three compelling reasons for long-term investors to view Ford as an attractive proposition, notwithstanding its present-day hurdles.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.