Amidst the recent market rally, investors have experienced minimal gut-check moments. However, we find ourselves entrenched in one such moment.

Even with the recent declines, the S&P 500 still boasts a gain of over 13% post yesterday’s close. The largest drawdown observed this year was around 6%, occurring back in April during the traditionally bullish month of spring.

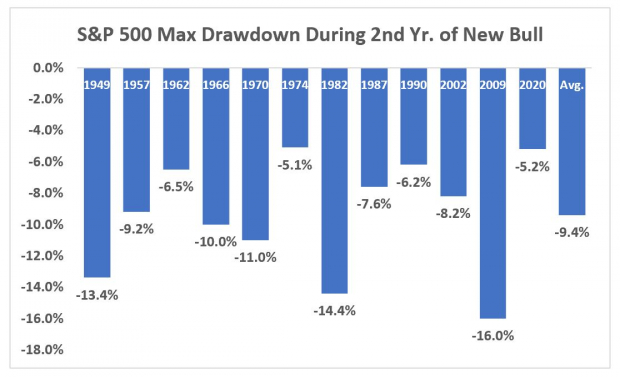

Historically, the average drawdown in the second year of a new bull market stands at 9.4% (referencing the beginning years of new bulls).

While conventional wisdom hints at a probable sharper pullback in the September-October period due to seasonality, the unpredictability of the stock market renders anything possible. Reacting hastily to short-term price fluctuations is a slippery slope.

Contemplating the seasonal outlook, the current market volatility could potentially pave the way for an uptick as we transition into August. It’s imperative to base investment decisions on facts, not emotions. Seasonal data suggests an increased likelihood of strength next month.

Remarkably, August historically stands strong in election years, and the recent market softness might merely signify overdue selling pressure amidst initial earnings season nerves.

Key Inflation Measure Indicates Downtrend

U.S. stocks rebounded in early trading on Friday, inching towards reclaiming crucial levels as investors embraced fresh data reinforcing the declining inflation trend.

The June Personal Consumption Expenditures (PCE) index noted a 2.5% year-over-year rise, aligning with economists’ forecasts. The index inched up 0.1% on a monthly basis, also meeting estimates.

The “core” PCE, excluding food and energy costs – the Fed’s preferred inflation barometer, showed a 2.6% increase over the previous year. Though slightly above the median projection of 2.5%, this reading represented the slowest yearly uptick in over three years. The persistent disinflation strengthens the case for imminent interest rate cuts.

The Federal Reserve’s forthcoming monetary policy decision is slated for July 31st. While the market currently prices in a mere 5% likelihood of a cut next week, the odds of a rate reduction have surged to 100% for the September meeting.

Second-Quarter Earnings Season Gains Momentum

The second-quarter earnings season is now in full swing. Given the robust market rally leading up to the season, encountering some turbulence as results stream in is unsurprising.

With the S&P 500 down around 4% since July 16th, it appears this adjustment phase is underway. Such sell-offs may set the stage for seasonal resilience moving into August.

Of the S&P 500 companies, 134 have disclosed their Q2 results, representing roughly 26.8% of the index. Overall earnings have seen a 7.6% uptick from the same period last year on 4.7% higher revenues.

Projections indicate total Q2 earnings could rise by 9.6% compared to the previous year, coupled with a 4.9% revenue increase. This would mark the most robust earnings growth since the 10% surge witnessed in Q1 of 2022.

Market Outlook and Final Insights

Next week anticipates a flurry of earnings announcements, particularly in the tech sector, with four of the “Mag 7” members expected to reveal their results. Microsoft, Facebook-parent Meta Platforms, Apple, and Amazon are all on deck.

A notable positive amidst recent turbulence has been the outperformance of small-caps, with the Russell 2000 gaining momentum in recent sessions. The more sustained this movement proves, the more significant it becomes.

Market breadth has exhibited unexpected resilience during the recent decline. Notably, on Wednesday’s downturn of over 2% in the S&P 500, a third of the stocks within the index actually saw gains. This marked the best breadth on a 2% down day since October 2000.

Interestingly, the volatility (VIX) index is retracing from a three-month peak. Given the prevailing “buy the dip” market sentiment this year, capitalizing during occasional spikes in volatility has been the prudent approach. The upcoming trajectory of stocks as we delve deeper into the Q2 earnings season remains to be seen.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.