Spotify Technology S.A. (SPOT) is set to unveil its second-quarter 2024 financial results on July 23, before the markets open.

Analysts project earnings of $1.1 per share for this quarter, a notable recovery from the $1.69 loss per share recorded in the same period last year. Revenue estimates point to $4.1 billion, marking an 18.7% growth year-over-year.

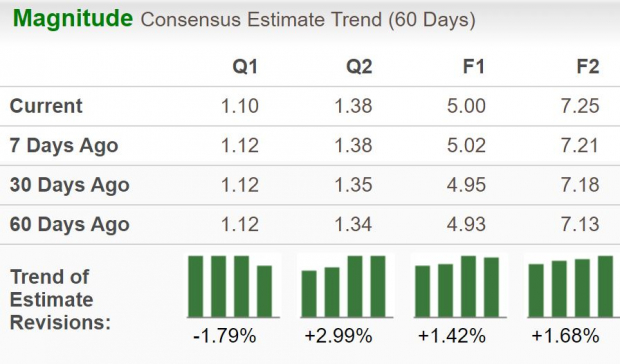

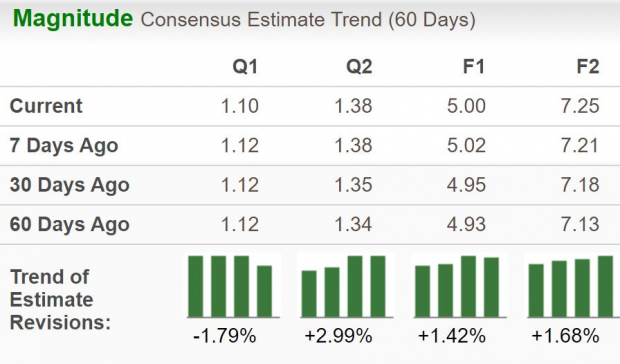

While two estimates for the upcoming quarter have been revised downwards in the last month, no upward revisions were noted. Additionally, the consensus estimate for 2024 earnings has dipped by 1.8% over the same period.

Image Source: Zacks Investment Research

In terms of earnings surprises, Spotify has had a mixed history. While outperforming estimates twice, it fell short on two occasions, with an average negative surprise of 40.2%.

Unveiling Spotify’s Price and EPS Performance

Discover more about Spotify Technology’s price and EPS performance.

Insights into Earnings Expectations

Prognosticators are divided this time regarding Spotify’s earnings beat. A positive combination of Earnings ESP and a Zacks Rank of #1, #2, or #3 typically bodes well for an earnings beat. However, the current scenario does not align with these criteria, with Spotify sporting an Earnings ESP of -9.70% along with a Zacks Rank of #1.

Factors Driving Anticipated Results

The expected surge in subscribers and monthly active users (MAUs) is anticipated to propel revenue growth in the upcoming quarter, consequently impacting the bottom line positively.

Estimates outline a 10% year-over-year increase in total MAUs to 631.3 million, a parallel rise of 10% in total ad-supported MAUs to 396.7 million, and an 8.5% growth to 245.3 million premium subscribers.

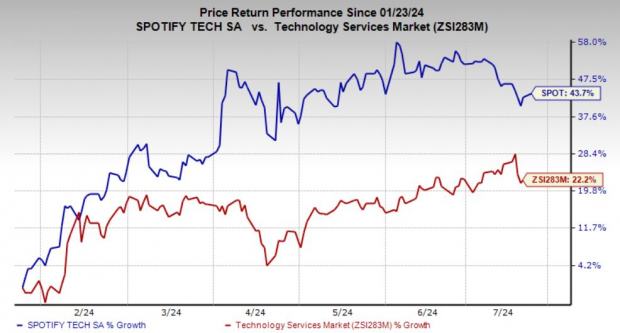

Stock Performance Dynamics

While Spotify’s stock witnessed a substantial 43% upswing over the past six months, it experienced a downturn of 3% and 6% in the last three and one months, respectively. These fluctuations hint at a corrective phase for the stock.

Image Source: Zacks Investment Research

Investment Insights

Spotify has displayed robust performance metrics, driven by consistent price hikes, a dedicated consumer base, and significant cost reductions in 2023. These price adjustments have not only elevated the top and bottom-line growth for Spotify but have also underlined its ability to attract and maintain a loyal user base. The consistent growth in MAUs and premium subscribers further solidifies Spotify’s market position.

Hence, the upcoming quarter is expected to reflect strong performance buoyed by subscriber gains, improved Average Revenue per User (ARPU), and subsequent positive impacts on the bottom line and overall financial health.

The music streaming industry has witnessed multiple price hikes among Spotify’s competitors, including Alphabet’s YouTube Premium, Apple’s Music/TV, and Amazon’s Music Unlimited.

In Closing

Despite recent corrections in its stock value, Spotify remains fundamentally robust. The company’s resilience stems from sustained price adjustments, a loyal customer base, and substantial cost-saving measures. In light of Spotify’s strong financial health and promising growth prospects, it emerges as a compelling investment opportunity within the music streaming sector, particularly amidst the ongoing earnings season.

Keep abreast of impending earnings updates through the Zacks Earnings Calendar.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.