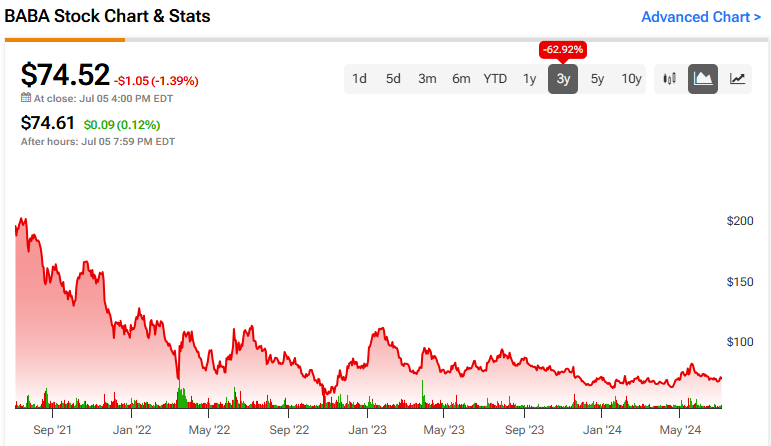

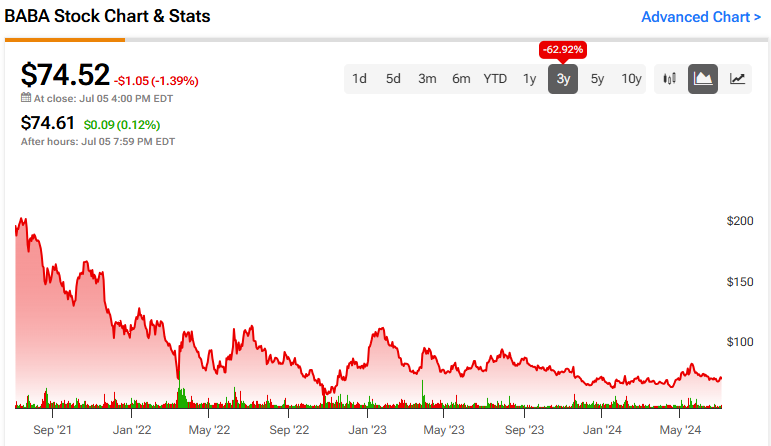

Alibaba stock (NYSE:BABA) has endured a prolonged period of despondency, showing no signs of a meaningful resurgence. While major market indices have reached new pinnacles in the past year, investor enthusiasm for the Chinese e-commerce behemoth’s prospects has remained tepid. However, recent indicators point to an acceleration in Alibaba’s growth trajectory. Additionally, a renewed corporate focus on enhancing capital returns, particularly through robust buyback initiatives, suggests a potentially bullish resurgence for the stock. Consequently, a newfound optimism has emerged in my assessment of BABA stock.

Growth Momentum Gains Traction, Paving the Way for a Resilient FY2025

Alibaba’s recent performance underscored a rejuvenated phase of growth, setting the stage for a resilient FY2025. The company’s Q4-2024 results, concluding on March 31st, showcased revenues of $30.7 billion, marking a 7% year-over-year upturn. This boost elevated Alibaba’s annual revenues to $130.4 billion, reflecting an 8% surge compared to FY2023. Notably, this rebound marked a stark contrast to the prior year, where revenues had stagnated at a mere 2% growth rate.

Across the board, Alibaba’s growth was fueled by robust traction. Core e-commerce platforms like Taobao and Tmall witnessed a 4% revenue uptick year-over-year, propelled by an expanded buyer base and heightened purchase frequency. The surge in gross merchandise value (GMV) on these platforms, driven by escalating order volumes, enhanced user experience, and competitive pricing strategies, achieved a double-digit growth rate.

Internationally, Alibaba International Digital Commerce (AIDC) exhibited a remarkable 45% revenue surge. The firm recorded robust combined order growth, revenue contributions from AliExpress’ Choice, and augmented monetization efforts, solidifying Alibaba’s global foothold.

Although Cloud Intelligence revenues experienced a more modest 3% growth vis-à-vis the previous year, notable advancements position this segment for accelerated growth in the near to mid-term. Alibaba registered double-digit revenue expansion in its core public cloud offerings and triple-digit growth in AI-related revenues.

With mounting evidence implying Alibaba’s pivotal role in China’s AI landscape, the company stands poised to dominate this sector domestically. This local advantage, stemming from its cloud computing prowess, creates a formidable competitive edge, reinforcing the bullish narrative.

Profitability Surge, Valuation Dynamics, and Strengthened Capital Returns

Alibaba’s resurgence in FY2024 catalyzed significant profitability enhancements, primarily attributed to the company’s exceptional economies of scale. Noteworthy achievements included a 12% growth in adjusted EBITA to $22.9 billion, alongside an expanded adjusted EBITA margin from 17% to 18%. Moreover, Alibaba’s adjusted net income ascended by 11% to $21.8 billion, translating to a more substantial 14% rise on a per-American Depositary Share (ADS) basis, bolstered by reduced ADS count resulting from Alibaba’s buyback initiatives.

Analysts anticipate a moderation in Alibaba’s ADS performance this year, with consensus estimates projecting $8.20 for FY2025, signaling a marginal decline of 4.7%. Despite this projection, Alibaba’s stock continues to trade at an unusually low forward P/E ratio of 9x. While acknowledging the well-documented risks associated with Alibaba, the stock’s compelling valuation beckons a revisitation of its investment proposition, given its formidable market position.

Notably, Alibaba’s escalated focus on capital returns underscores management’s response to the stock’s undervaluation, aimed at rewarding existing investors and enticing new ones through bolstered confidence. The company’s substantial share repurchases, retiring nearly 11% of its shares since early 2022, coupled with this year’s dividends, comprising regular and special payouts totaling $1.66 per ADS, offer an additional yield of 2.2% at current price levels.

With ample leeway for Alibaba to further enhance its capital return initiatives, the combined yield from repurchases and dividends assumes increasing appeal if the stock maintains its current valuation. The stock’s existing high single-digit total yield, supplemented by tangible capital returns, emerges as a formidable bullish catalyst that demands due recognition.

Analyst Consensus and Investment Implications

Wall Street analysts maintain a predominantly bullish stance on Alibaba, mirroring the stock’s discounted valuation. The Strong Buy consensus rating, grounded on 14 Buy ratings and three Holds, aligns with this sentiment. At an average price target of $103.70, recent projections surpass the current stock price, signaling an enticing upside potential of 39.2%.

Concluding Thoughts

Alibaba’s stock has weathered a prolonged spell of underperformance, even amidst broader market upswings. Nonetheless, recent developments portend a potential inflection point. With a resurgence in FY2024 and promising indicators for FY2025, Alibaba’s investment thesis appears increasingly compelling. Coupled with a renewed emphasis on capital returns, featuring substantial share repurchases and a burgeoning dividend stream, Alibaba stands poised to rekindle bullish sentiment.

Irrespective, at its prevailing valuation, the anticipated rewards seem to outweigh the risks, notwithstanding the inherent uncertainties accompanying an entity like Alibaba.

For more information, please refer to the full disclosure here.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.