Nvidia (NASDAQ: NVDA) has traversed a tumultuous path over the past half-decade. From navigating the downfall precipitated by the cryptocurrency market crash to now scaling remarkable peaks, Nvidia’s graphics processing units (GPUs) have emerged as indispensable tools for sculpting artificial intelligence (AI) models.

Speculating on Nvidia’s trajectory in the coming five years is akin to forecasting the weather in an era of climate change; uncertainty reigns. However, crafting an investment thesis for this tech titan, currently at the vanguard of the market, is not just prudent but imperative.

The Competitive Landscape for Nvidia’s Superior GPUs

Nvidia’s GPUs stand unrivaled as the crème de la crème, the top tier of excellence. The allure of Nvidia GPUs lies in their prowess to conduct multiple calculations concurrently, a godsend for crafting AI models. Nevertheless, this aura of exclusivity may dim.

While GPUs excel in creating AI models, alternative hardware offers superior efficiency for such tasks. Google Cloud’s tensor processing unit (TPU) shines in AI model training when the workload is optimized for the TPU. This evolution poses a potential threat to Nvidia’s dominion.

Custom-designed AI chips, like TPUs, emerge as challengers to Nvidia’s throne, with giants like Amazon Web Services, Microsoft Azure, and Meta Platforms embracing in-house chip creations. This paradigm shift may usher in a trial for Nvidia over the next half-decade, as its key clients venture into proprietary chip design territory.

On the flip side, Nvidia’s recent surge in GPU sales heralds an inevitable replacement cycle. With GPUs typically boasting a lifespan of three to five years in data centers, a wave of product replacements looms on the horizon, akin to a phantom ready to strike at the core.

The inexorable demand for computing power ensures the perpetual use of these GPUs; disposal isn’t an option. This cyclical pattern spawns a quasi-subscription effect, anticipating a forthcoming wave of product renewal for Nvidia in five years.

Technological strides in chip innovation, epitomized by Taiwan Semiconductor’s forthcoming 2-nanometer chip technology, breed optimism for Nvidia’s future. These advancements promise more potent and energy-efficient GPUs, augmenting long-term benefits for its clientele.

Yet, as we gaze into the crystal ball, the burning question lingers: Is the stock price a harbinger of all these impending transformations?

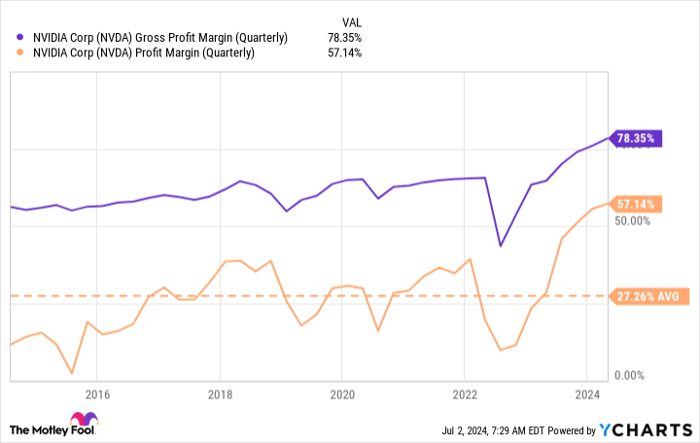

Nvidia’s Profit Margins: The Precarious Challenge

Nvidia’s stock stands as a beacon of premium valuation, trading at 73 times trailing earnings and 46 times forward earnings, embodying the burden of anticipated vigorous growth.

Concealed in the shadows lurk Nvidia’s staggering margins, hovering around the 60% mark, a rare feat that often eludes discussion. These superlative margins serve as a magnet for companies venturing into custom chip design realms.

The current frenzy for Nvidia GPUs empowers the company to command a premium price for its products. However, this scenario is transient, and in due course, the halo may dissipate, heralding a probable dip in profit margins over the ensuing half-decade.

As the tides turn, and Nvidia grapples with heightened competition from in-house solutions, a subtle shift in its price-to-earnings (P/E) ratio looms. The stock faces the risk of an impending reality check, refuting the market’s unwavering belief in perpetual revenue ascension.

Even though the hunger for Nvidia’s wares is poised to endure, the encroaching challenge of in-house solutions portends stormy weather ahead. A sage adage resonates — a company’s margins are a rival’s opportunity, foreshadowing impending competition as Nvidia’s margins draw competitors nearer.

Consequently, Nvidia’s stock may weather tumult over the coming quinquennium. The fervor driving current demand may ebb, beckoning companies to the table where Nvidia’s bounty garners a watchful gaze, primed for a possible plunder.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.