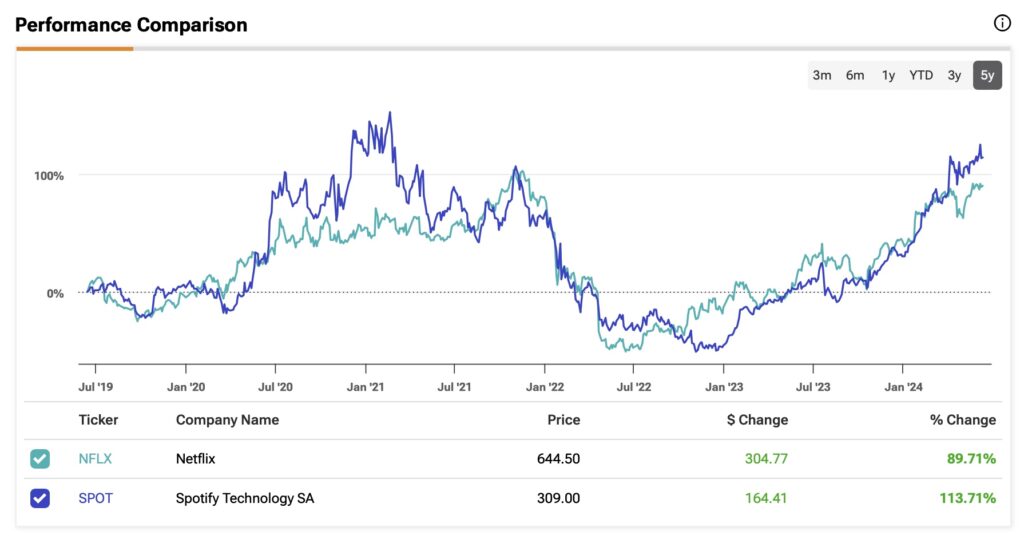

In the world of streaming, two behemoths, Netflix and Spotify, stand tall, commanding attention and speculation from investors. Netflix, listed on NASDAQ as NFLX, and Spotify, on NYSE as SPOT, have traversed tumultuous market terrains, experiencing ebbs and flows akin to a tempestuous sea.

Distinct Business Models in the Streaming Arena

Netflix and Spotify, although players in the same streaming space, wield divergent swords in their quest for dominance. Netflix, the pioneer, birthed from a focus on licensing that metamorphosed into a colossus emphasizing exclusive original content. On the other shore, Spotify, navigating the audio streaming realm, dances delicately, unable to craft its own tunes and reliant on brokered deals with music maestros.

Subscription revenues form the bedrock for both titans, Netflix supplemented tentatively by an ad-supported plan and Spotify humming tunes of free ad-generated income. Each path laden with boons and banes, as Netflix’s subscriber-driven model contends with costly content creation, juxtaposed against Spotify’s escalating licensing bills tethered to stream numbers.

Clash of Titans in the Streaming Colosseum

The coliseum of streaming witnesses gladiators Netflix and Spotify engage in a ferocious battle for supremacy, egged on by an audience shifting swiftly from old-world cable to the digital domain. Amidst this maelstrom, giants such as Amazon and Apple hover, investing billions in content without sight of immediate profit.

Netflix, reigning with a lion’s roar, claims the video streaming crown, holding court as the second-largest entity by market share, outstripped only by YouTube’s ad-driven specter. Spotify, the maestro of sound, commands over 31% of music streaming’s aristocratic realm, though challenged with a gradual erosion of its empire.

Unveiling Growth Trajectories and Value Narratives

In the saga of growth, Netflix’s tale spins a yarn of a 9.8% compound annual growth dance, while Spotify’s ballad sings of a brisk 19% pace. Yet, the chasm lies in the profit margins’ domain, with Netflix’s hoisting itself at a lofty 46%, casting a shadow over Spotify’s modest 28% midst.

Embracing valuation lenses, peering into the crystal ball reveals Spotify treading at a perplexing crossroads bearing a P/E yoke of 65x, while Netflix’s P/S cloak shimmers at 8x. A discount tale borne by Spotify’s hesitance to solidify its model, juxtaposed with Netflix’s steady strides into profitability sanctuary.

The Analyst Oracle: What Do the Stars Foretell for NFLX?

Wedbush’s bard, Alicia Reese, heralds Netflix, flagging the company’s premium perch with strategic maneuvers unfurling avenues of revenue diversification. Ad solutions, partnerships sprouts, and the specter of live events conjure images of burgeoning ad-tier bounties, steering the barge towards cash-laden waters.

Amidst the Wall Street soothsayers, a Moderately Buoyant consensus breeze envelops Netflix, with 23 seers beckoning Buy, 12 Hovering Hold, and a Solemn Singleness singing Sell. The incantation of a $657.98 per share price target weaves a tapestry tinged with a mere 1.7% downside tint.

Decoding Streaming Giants: A Critical Analysis of NFLX and SPOT

Evolution in the Streaming Sphere

The labyrinthine world of streaming services unveils a complex tapestry of competition, innovation, and financial prowess. In this dynamic landscape, Netflix and Spotify emerge as titans, each reigning over distinct realms of video and music streaming, respectively.

While both companies depend heavily on subscriber revenue streams, the nuances in their business models delineate significantly. Netflix, enshrined in the denser realm of competition, flaunts resilient margins and an upward trajectory in revenue growth.

Conversely, Spotify, as a behemoth in music streaming, grapples with the intricacies of profitability. Despite commendable strides in recent times, the sanctuary of profitability still eludes the music maestro. Escalating licensing expenses tether Spotify’s margins, contrasting with Netflix’s profitability paragon fortified by in-house creations.

Analyzing Financial Projections

Within this tumultuous clash of industry giants emerges a tale of contrasting fortunes, mirrored in stock projections. Maria Ripps from Canaccord Genuity heralds an optimistic forecast for Spotify. The symphony of raised subscription prices in the U.S. and stringent cost-cutting endeavors orchestrates a sonnet of margin enhancement—an allegro to the investors’ ears.

Analysts reverberate Ripps’ optimism, casting a moderate buy on Spotify. Of the 26 whisperings in the analyst corridors, 19 proclaim a buy, while seven opt for a holding pattern. The average price target, resonating at $353.39 per share, sings a sweet melody of potential—a crescendo promising a 12.9% rise.

Oscillating Narratives: NFLX vs SPOT

Amidst the swirling tempest of market sentiment, one question echoes louder—NFLX or SPOT? As investors navigate this melodic labyrinth, NFLX emerges as the conductor of stability, orchestrating a symphony of solid, sustainable performance. The premium valuation demanded is a paltry fee for the fortress of Netflix’s business.

Contrariwise, Spotify, perched atop the music pedestal, oscillates between struggles and successes. The silver lining of profitability glistens on the horizon, albeit distant. Spotify’s slender margins, enfeebled by licensing costs, juxtapose Netflix’s profitable valor delivered through internal productions.

Despite Spotify’s alluring P/S ratio, Netflix presents itself as the colossus of reliability, a beacon in the tumult. Hence, the scales tip in NFLX’s favor, casting a shadow of doubt on SPOT’s path to sustainable profitability.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.