Nvidia(NASDAQ: NVDA) recently shattered records as only the third U.S. public company to breach the $3 trillion market cap milestone. This remarkable achievement follows in the notable footsteps of Apple in January 2022 and Microsoft in January 2024. With a groundswell of investors anticipating Nvidia’s eventual dethronement of Microsoft in the market cap realm, the chipmaker’s trajectory is a source of fervent speculation.

Delving into the factors propelling Nvidia stock to these unprecedented heights and exploring the company’s future trajectory is paramount for astute investors.

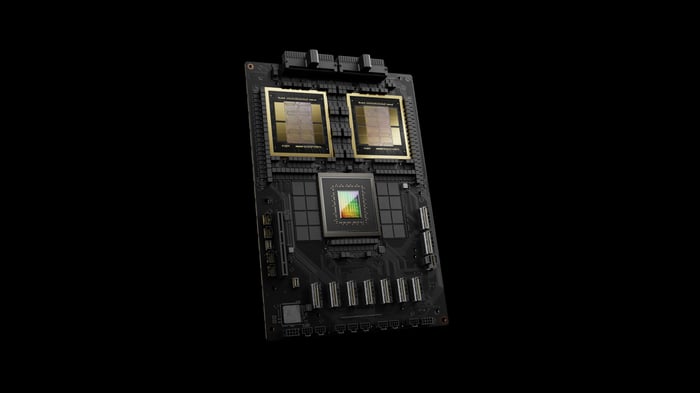

The Nvidia GB200 Grace Blackwell Superchip. Image source: Nvidia.

Legendary Status in the Chipmaking Industry

Nvidia’s recent successes are intrinsically tied to the explosion of interest in artificial intelligence (AI) that has swept through various sectors. However, it’s crucial to glance back at a time when Nvidia faced a stark downturn: Between November 2021 and October 2022, Nvidia stock plummeted by over 66% amidst macroeconomic turbulence. Gamers clung to outdated graphics cards, and businesses exhibited a lack of inclination towards updating their data centers.

As the saying goes, “This too shall pass.” The emergence of generative AI in early 2023 catalyzed a technological paradigm shift, with investors swiftly recognizing that Nvidia’s data center chips lay at the core of the AI revolution.

Generative AI, a cutting-edge branch of AI capable of crafting original content, marked a fundamental departure from previous iterations. These AI models could compose poetry, craft new music, generate paintings, and more. Technologists soon realized these systems could streamline tasks such as drafting emails, creating presentations, and debugging code, enhancing worker productivity and saving businesses invaluable time and resources.

Nvidia’s key to success lies in the parallel processing capacity embedded in its graphics processing units (GPUs). Simplified, parallel processing disassembles complex computational tasks into manageable chunks, expediting daunting assignments. Leveraging this technology’s prowess from earlier AI iterations, Nvidia seamlessly transitioned when generative AI beckoned.

However, these AI models, each laden with trillions of training data bits termed parameters, necessitate thousands of GPUs. Training a single AI model like OpenAI’s GPT-4 demanded over 25,000 of Nvidia’s top-tier A100 AI processors, each priced at $10,000 – translating to a staggering $250 million for one model. This cumulative expenditure across cloud infrastructure providers, data centers, and global enterprises eyeing the AI domain illuminates the immense potential.

A Legacy of Triumph

Nvidia’s current zenith stems from CEO Jensen Huang’s visionary foresight. Although AI now reigns supreme, the landscape differed in 2013 when Huang pivoted Nvidia towards embracing this nascent technology.

Mirroring lifelike image rendering for video games, parallel processing – foundational to Nvidia – was harnessed to tackle AI’s demands. Subsequently, the company’s trajectory began shifting dramatically.

Eclipsing victories predated generative AI’s rise to prominence, yet AI now fuels Nvidia’s prosperity. Over the past decade, Nvidia’s revenue catapulted by 2,260%, bolstering a staggering 11,530% surge in net income. This upswing propelled a 27,900% surge in its stock price, with many believing that the company’s prime has not yet been reached.

Data by YCharts

Preceding its meteoric rise, Nvidia is poised to undergo a 10-for-1 stock split, scheduled post-market closure on Friday. Research by Bank of America’s Jared Woodard indicates that companies partaking in share splits typically witness a 25% increase – compared to the S&P 500’s 12% gain – within the ensuing year. This augmentation is likely a manifestation of the operational and financial excellence fueling the previous stock price surge, catalyzing the split.

Recent fiscal highlights from Nvidia depict a compelling narrative. In its fiscal 2025 first quarter (ending April 28), Nvidia surmounted a 262% revenue increase year-over-year, ascending to a record $26 billion. Simultaneously, earnings per share surged by 629% to $5.98, buoyed by the data center segment – inclusive of AI processors – witnessing a staggering 427% revenue surge to $22.6 billion, spurred by burgeoning AI chip demand.

Predicting Nvidia’s Trajectory

Recent months reveal investors grappling with AI’s sustainability, adopting a cautious “wait and see” stance, although this reserve might prove costly. Conservative estimates project the generative AI market size at $1.3 trillion by 2032, as proposed by Bloomberg Intelligence. Conversely, Ark Invest’s CEO Cathie Wood envisions a robust total addressable market of $13 trillion by 2030. The veracity likely resides between these extremes, indicating the unpredictable size of the AI landscape.

Foremost tech giants are fervently crafting Nvidia’s GPU competitor with limited success thus far. Concurrently, Nvidia’s robust investment in research and development (R&D) – amounting to nearly $8.7 billion last year, constituting 14% of its total expenditure – reinforces the company’s commitment to retaining AI processor supremacy.

Unveiling the Dynamics of Nvidia in the Tech Terrain

With more than a decade-long head start and continuing large expenditures on R&D, it’s going to be tough for its rivals to “chip” away at Nvidia’s leadership. The competition is coming, but the size of the market suggests there can be more than one winner.

It’s essential to recognize that a $3 trillion market cap benchmark is entirely arbitrary. Investors would be wise to focus on Nvidia’s operating and financial results, which have remained consistently stellar, providing valuable insights into the company’s ongoing prospects.

Moreover, a note on valuation is prudent. The surge in Nvidia’s stock price in recent years has propelled its valuation to a level that many investors find discomforting. Currently trading at 72 times earnings and 38 times sales, some deem this valuation excessive. However, overlooking Nvidia’s triple-digit growth over the past four quarters, a trajectory expected to persist into the current quarter, would be myopic. Notably, Nvidia’s price/earnings-to-growth (PEG) ratio, factoring in this growth, stands at less than 1, meeting the standard for an undervalued stock.

Contrarians may highlight the looming threat of competition, the lofty stock price, and the uncertain future of AI. Nevertheless, Nvidia stands as the most assured path to claim a share of the windfall offered by AI technologies. In my estimation, this perspective renders Nvidia stock a compelling investment proposition.

Exploring Nvidia’s Investment Appeal

Before considering an investment in Nvidia, ponder the following:

The Motley Fool Stock Advisor analyst team has recently pinpointed what they deem the 10 best stocks for investors to acquire now… and Nvidia didn’t make the cut. The 10 selected stocks hold the potential to yield substantial returns in the forthcoming years.

Reflect on Nvidia joining this list back on April 15, 2005 — an investment of $1,000 at the time of the recommendation would have multiplied to a remarkable $713,416!*

Stock Advisor equips investors with an easily understandable blueprint for success, offering guidance on portfolio construction, frequent updates from analysts, and bi-monthly stock picks. Noteworthy, the Stock Advisor service has outperformed the S&P 500 by more than four times since 2002*.

See the 10 stocks »

*Stock Advisor returns as of June 3, 2024

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.