Analyzing PayPal’s Dwindling Fortunes

PayPal’s once soaring trajectory has dipped, with a lackluster YTD gain of 4.4%, trailing behind the S&P 500 Index in 2024. This slump is not an anomaly, as the stock has been mired in underperformance for the past three years, missing out on the tech stock rally. The fintech giant witnessed a substantial decline, shedding three-fourths of its market cap within this timeframe, reaching multi-year lows before a tepid rebound.

Delving into the Causes of Underperformance

PayPal’s growth story is losing its sheen, with both top and bottom-line figures displaying signs of stagnation. Although Q1 of 2024 saw a 9% YoY revenue increase, full-year sales projections for 2024 and 2025 hover around 7.5% to 8.1%, indicative of a sluggish pace. Profit growth remains subdued, with the 2024 EPS expected to eke out gains in the mid-to-high single digits.

Compounded by escalating competition, digital payment firms are grappling with shrinking take rates. PayPal’s GAAP operating margin, which stood at 18.1% in Q2 2020, suffered a decline, plummeting to 15.2% by Q1 2024.

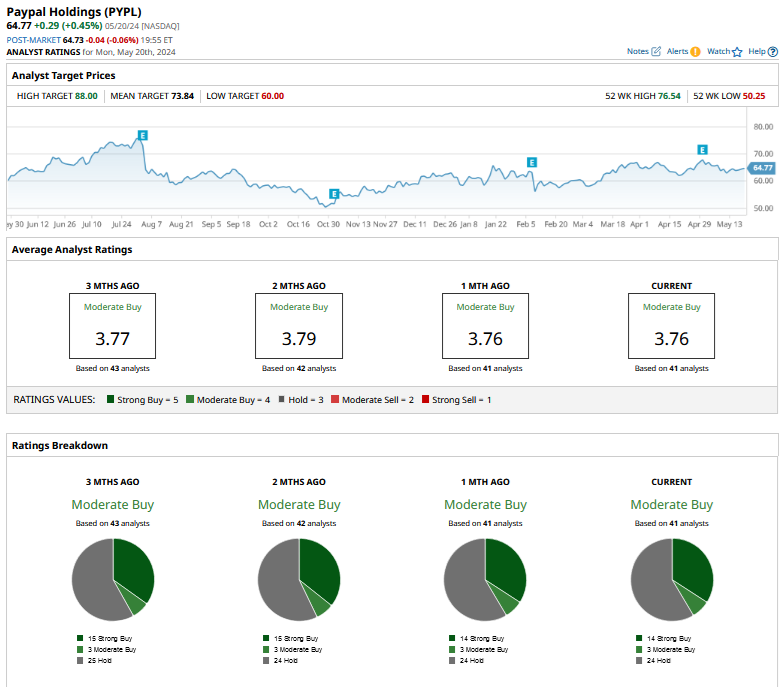

Forecasting PayPal’s Trajectory

Market analysts opine that PayPal deserves a “Moderate Buy” rating, reinforcing a tepid confidence among investors. A mean price target of $73.84 reflects a 15% premium over the current prices, while a street-high target price of $88 indicates a substantial 37.3% valuation boost.

Redefining PayPal’s Market Image

Embracing a shift in leadership, PayPal’s appointment of Alex Chriss as the CEO aimed to steer the ship toward profitable growth and innovation. However, these measures failed to resonate with stakeholders, relegating PayPal from its erstwhile growth pedestal to a value stock. Trading at a relatively modest NTM P/E ratio of 15.7x, PayPal anticipates generating $5 billion in free cash flows for 2024.

The Dividend Debate: To Pay or to Repurchase?

In a landscape where tech firms seldom dish out hefty dividends, PayPal finds itself in a conundrum. With stalwarts like Meta Platforms and Alphabet venturing into dividend territory, rumblings suggest PayPal may follow suit. Financially robust, boasting a favorable debt position and healthy cash reserves, PayPal could cater to a dividend-seeking investor base by initiating payouts.

Nonetheless, the timing seems ill-suited for a dividend debut. Encumbered by a “transition” phase, PayPal’s focus on business reformation takes precedence. In cognizance of suppressed valuations, a strategy favoring share repurchases emerges as a prudent choice. The company earmarks $5 billion for buybacks, an amount mirroring its projected free cash flows for 2024.

Though a dividend may beckon on the horizon as PayPal matures further, the present juncture appears propitious for bolstering valuations through share repurchases.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.