During roaring bull markets, investors often delve into benchmarking – comparing their portfolio’s performance against a major index. While this practice is widely encouraged by Wall Street and the media, is benchmarking truly beneficial for you?

Let’s explore why Wall Street advocates for comparing performance to a benchmark index.

The urge to compare, driven by societal norms and media influence, can lead to unrest and insecurity. In the financial realm, this comparison can often result in ill-advised decisions.

The continuous measurement against arbitrary benchmark indices often derails investors, preventing them from adhering to their chosen investment strategies.

Clients may be content with a 12% return on their account until realizing that others achieved 14%, causing dissatisfaction. The financial services industry thrives on this discontent, prompting frantic movement of investments.

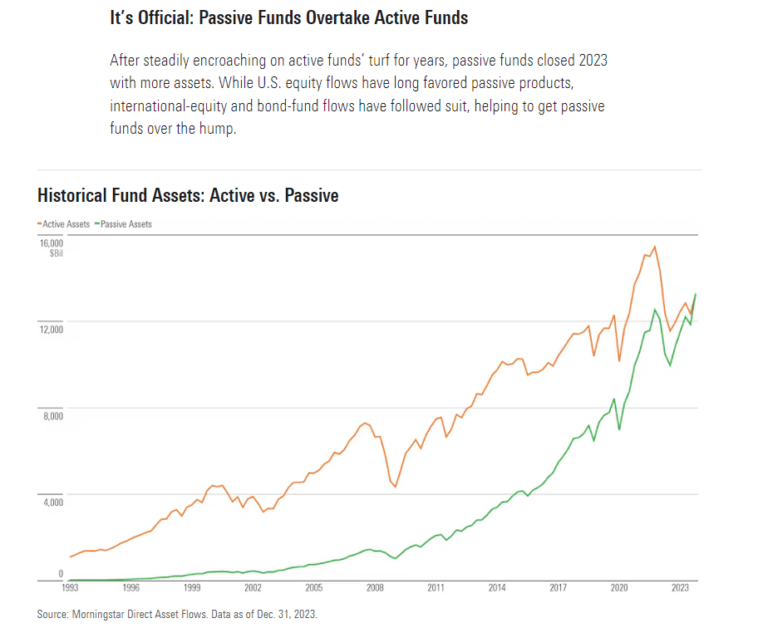

The industry’s emphasis on benchmarking and indexing has intensified, pushing investors towards passively managed funds as actively managed ones struggle to outperform. This shift has led to a concentration of assets in a few dominant companies, posing a significant risk.

The Pitfalls of Market Cap Weighting

When investors or advisors construct portfolios and compare them to an index, they expose themselves to substantial risks, especially in today’s market environment. This peril stems from the concentration of assets in top-performing stocks, fuelled by passive investing trends.

The influx of investments into passive index funds elevates the market capitalization of select companies, posing a risk to portfolios that do not mirror this concentration.

Consider this: when $1 is invested in the S&P 500 index, $0.35 directly flows into the top 10 stocks, magnifying the risk of portfolios not aligned with these giants.

Striving to outperform the index annually is an even tougher challenge, as evidenced by the rarity of prolonged success stories like Bill Miller’s 15-year streak of beating the S&P 500.

Navigating Portfolio Management for Sustainable Success

Mainstream benchmarking often fixates on short-term performance, neglecting the subtleties of long-term investment strategies. While buying an index guarantees underperformance due to operating costs, well-managed portfolios can surpass indices over extended periods with lower risk.

Contrary to the one-year comparison, a meticulously crafted investment strategy can yield superior returns over extended periods, outranking the S&P 500’s growth. Identifying funds with established track records is challenging, considering many emerged post the late ’90s boom.

Diving into long-term performance analyses of mutual funds like Fidelity Magellan and others against the S&P 500 reveals that actively managed quality funds can outshine indices without heavy reliance on a few stocks.

Quality, actively managed funds over the long haul seem to offer a more secure investment avenue, circumventing the pitfalls of narrowing stock concentration.

Financial Resource Corporation aptly summarizes this approach as preferring consistent above-average returns over time, positioning investors favorably against the majority of their peers.

The Nuances of Portfolio Performance: A Closer Look

There are countless pitfalls in the financial world, particularly when comparing one’s investment portfolio to benchmark indices. As the age-old adage goes, “apples to oranges.” When scrutinizing the performance of investment funds against benchmarks like the S&P 500, investors can easily fall prey to the illusion of uniformity.

The Only Thing That Matters

Over time, chasing after index performance becomes a mesmerizing dance that often leads to skewed assessments. Statistics such as “80% of all funds underperform the S&P 500” can deter investors from exploring more diverse and potentially fruitful strategies. The allure of share buybacks, tax advantages, and other index-specific perks can blind investors to the merits of diversified portfolios.

While benchmark indices like the S&P 500 boast impressive gains, they often necessitate a high-risk appetite that may not align with individual investors’ goals. The quest for lower volatility, steady income, or long-term financial security can lead to underperformance when compared to the alluring index.

“But it gets worse. often times, these comparisons are made without even considering the right way to quantify ‘risk.’ That is, we don’t even see measurements of risk-adjusted returns in these ‘performance’ reviews. Of course, that misses the whole point of implementing a strategy that is different than a long only index.”

– Cullen Roche

Therefore, attempting to mirror the S&P 500 or any other benchmark index often results in a misalignment between investment strategies and personal financial objectives. This disconnect can spur emotional decision-making and excessive risk-taking, both of which are detrimental to long-term wealth accumulation.

“What’s more important – matching an index during a bull cycle, or protecting capital during a bear cycle?”

The crux of the active versus passive investment debate lies in this fundamental question. Striving to match index performance during bull markets may expose investors to significant losses in downturns. In contrast, prioritizing capital preservation during bear markets can safeguard one’s financial goals in the long run.

Investing is not a game of winning or losing; it’s a strategic endeavor aimed at securing future financial stability. Viewing investments through the lens of personal objectives and risk tolerance rather than benchmark indices is crucial for sustainable wealth growth.

In the grand scheme of things, outperforming the index may not be the ultimate goal. Instead, achieving individual investment milestones and securing future financial well-being should remain the focal point of any prudent investor.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.