Investors who have closely followed the trajectory of artificial intelligence (AI) stocks have recently found themselves in a quandary. Following a period of consistent growth lasting nearly a year, the AI segment experienced a cooling-off period in March. The subsequent pullback in certain stocks left investors pondering whether the AI rally had reached its zenith or whether it was simply a necessary short-term recalibration.

Depending on the individual company, the recent sell-offs were likely ephemeral corrections. Seeking to navigate these fluctuations, we consulted with three Motley Fool analysts. Here are our insights on three AI stocks that now present promising opportunities for investors.

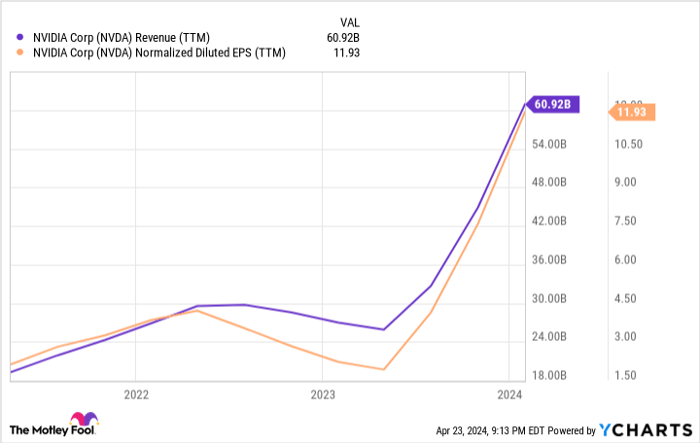

Nvidia: Weathering a Healthy Breather, Unveiling a Long-Term Buying Opportunity

Justin Pope (Nvidia): Nvidia (NASDAQ: NVDA) emerges as the top pick for capitalizing on the dip. While the stock has seen explosive growth in recent years, its triple-digit percentage growth in revenues and profits justified these gains. This uptrend in Nvidia’s business appears poised to endure for the foreseeable future.

Nvidia currently stands as a dominant player in the AI chip sector. The company’s success in capturing a vast portion of the market can be attributed to its state-of-the-art chips and proprietary software that optimizes computing performance. Analysts estimate Nvidia’s control of up to 90% of the AI chip market.

Looking ahead, the potential is clear. AI is primed to become a substantial market, with demand for computational power projected to double by 2030. Even if competitors chip away at Nvidia’s market share, the company stands to benefit from the increased demand resulting from this expansion.

Analysts forecast Nvidia’s earnings to grow at a rate of 35% annually over the next three to five years. Given the current share price, the stock boasts a reasonable PEG ratio of 1. Don’t be swayed by short-term price fluctuations; the likelihood is high that Nvidia will emerge as a more valuable stock in the years ahead. Zoom out for a broader perspective, and Nvidia’s intrinsic value will shine through.

Microsoft: Reaping Rewards from Early AI Investments

Jake Lerch (Microsoft): Microsoft (NASDAQ: MSFT) garners the spotlight as a prime candidate for investment, thanks to its early focus on AI that is beginning to bear fruit. Following a minor downturn in recent weeks, the opportunity to invest in the world’s largest company should not be underestimated.

Microsoft’s positioning in the cloud computing domain exemplifies its growth potential. While historically overshadowed by Amazon Web Services (AWS), Azure is now outpacing AWS in revenue growth. Microsoft has seamlessly integrated new AI tools into its offerings, including the Copilot suite, priced at $30 per month. In contrast, Amazon has yet to substantially incorporate AI features into AWS.

Unlike some AI-focused stocks, Microsoft’s value is not solely tethered to the performance of this niche sector. With diversified business operations spanning gaming to advertising, Microsoft mitigates investment risks. Moreover, Microsoft’s steadfast progress is evidenced by its ambitious revenue target of $500 billion by 2030, more than doubling its current figures.

CEO Satya Nadella’s track record speaks volumes, with Microsoft’s stock surging by an incredible 1,110% under his leadership. In summary, Microsoft endures as a formidable company worthy of consideration for investors seeking to benefit from any market dips.

Tesla: Defying Pessimism to Emerge as a Potent Investment

Will Healy (Tesla): Planting a flag amidst the prevailing negativity surrounding the stock, Tesla (NASDAQ: TSLA) emerges as a compelling choice to capitalize on the dip.

The Resilient Evolution of the Electric Vehicle Industry

An Electric Shock to the System

An electric vehicle (EV) giant has endured a turbulent ride, shedding nearly half its value since last fall, with its market cap plummeting by over 60% from 2021 peaks. A cocktail of factors – from waning EV sales growth to a sobering Cybertruck recall and uncertainties around a planned affordable vehicle – have shattered previously rosy projections, pushing the stock into a tailspin.

Financial Quagmire and Glimmers of Hope

In the wake of lackluster first-quarter results, where revenue dipped by 9% to $21 billion, and a 55% slump in quarterly net income to $1.1 billion, the company found itself at a crossroads. Operating expenses soared, creating a financial storm that needed a silver lining.

The Rise of AI and Robotaxis

Amidst this turmoil, a beacon of hope emerged in the form of artificial intelligence (AI). The firm’s forthcoming revelation of a robotaxi on August 8th resonated with investors. With recent enhancements to its self-driving software and a halved monthly fee, optimism flourished for the impending debut of the robotaxi.

Ark Invest’s Rosy Crystal Ball

The optimism was further fueled by the visionary Cathie Wood and her team at Ark Invest, who placed a lofty $2,000 per share price target for the EV behemoth by 2027, projecting a staggering 12-fold surge from current levels. Their past predictions have not been mere shots in the dark. Back in 2018, when Tesla’s split-adjusted price was a paltry $23 per share, Wood envisaged a soar to the modern equivalent of $267 per share, a milestone Tesla swiftly conquered in 2021 before facing setbacks.

A Bloom in the Desert

As Tesla gears up to kick off the production of a lower-cost vehicle in the latter half of 2025, the stock witnessed a revitalization, hinting at a possible nadir. The surging demand for budget-friendly EVs coupled with a growing pool of prospective customers eyeing robotaxis could sprout into enduring tailwinds for Tesla, possibly validating another audacious Ark Invest forecast.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.