As the financial landscape morphs in the current bull market, a cohort of technology giants have risen to prominence, akin to a modern-day “Magnificent Seven.” From this elite group emerged the formidable “Fab Four” of Nvidia, Amazon, Meta Platforms, and Microsoft.

Yet, as markets evolve, sticking solely to these tried and tested names may not be the wisest strategy. With substantial gains already under their belt, investors are now seeking novel avenues for growth. In this pursuit of fresh opportunities, three Motley Fool contributors advocate a deviation from the usual suspects, urging consideration for companies like the reclusive Tesla, the up-and-coming CrowdStrike, and even the wildcard entry, Lemonade.

Revving Up Tesla’s Potential with AI

Will Healy (Tesla): In the realm of affordable artificial intelligence (AI) stocks, overlooked gems can often yield unexpected value. Enter Tesla, a company currently weathering a storm due to a decline in EV sales. Amidst speculations about shelving plans for a budget-friendly Model 2, the stock has faced turbulence.

Yet, beneath this facade of adversity lies a hidden strength – Tesla’s AI-powered full self-driving platform. Recent enhancements to this technology, coupled with CEO Elon Musk’s revelation of an upcoming robotaxi debut on Aug. 8, signify a potential turning point. Cathie Wood’s Ark Invest envisions a lofty future for Tesla, foreseeing shares soaring to $2,000 by 2027, buoyed by the transformative potential of this robotaxi ecosystem.

Ark Invest identifies Tesla as a burgeoning player in the robotics domain, with the robotaxi poised to revolutionize both vehicle sales and the software-as-a-service platform powering it. By 2027, Ark Invest predicts that 67% of the company’s enterprise value will stem from robotaxis, contrasting starkly with the 85% revenue contribution from automotive sales in 2023.

While skeptics may abound, it’s worth recalling Ark Invest’s prescient forecast in 2018, when Tesla’s stock price surged to $267 per share by 2021, a tenfold increase as predicted. With Tesla’s P/E ratio hovering near a historic low at 40 post sell-off, a resurgence seems imminent as the company propels itself towards a technology-driven future.

CrowdStrike: Safeguarding Tomorrow’s Cyber World

Jake Lerch (CrowdStrike): In an era marred by perpetual cyber threats, cybersecurity solutions have assumed paramount importance. Enter CrowdStrike, a leading player in this arena, leveraging machine learning to avert network breaches before they materialize.

Amidst a backdrop of escalating cyber attacks, exemplified by the recent Change Healthcare hack, organizations are increasingly fortifying their digital ramparts. CrowdStrike’s innovative approach, underpinned by machine learning, has been pivotal in attracting a burgeoning clientele.

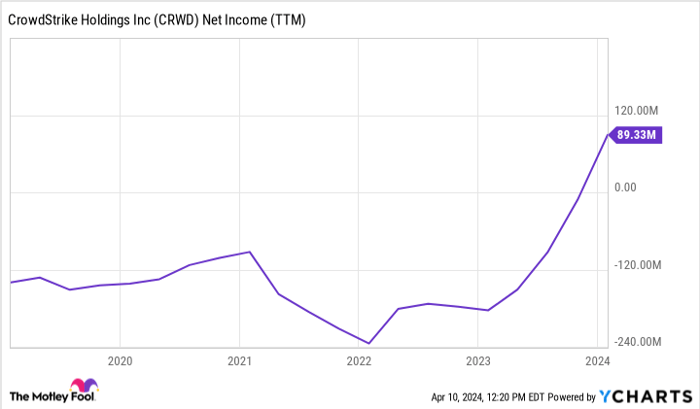

In its most recent fiscal quarter concluding on Jan. 31, CrowdStrike witnessed a 33% year-over-year revenue surge, with 94% of this staggering sum originating from subscription revenue. This subscription-based model fosters predictability, starkly contrasting with the volatility inherent in traditional sales.

Moreover, CrowdStrike is poised at a pivotal juncture in its trajectory, transitioning towards profitability. With a positive net income recently recorded for the first time, coupled with a soaring free cash flow of $3.81 per share, the financial outlook appears robust. This surge in free cash flow, often considered a barometer of long-term success, bodes well for CrowdStrike’s future financial performance and subsequent stock price trajectory.

As investors navigate the labyrinthine realms of the financial market, opportunities abound in unconventional avenues such as Tesla, CrowdStrike, and Lemonade, heralding a paradigm shift in investment strategies.

Lemonade’s Innovative Approach to Insurance

The insurance industry, long dominated by established giants with flashy commercials and traditional agent models, is ripe for disruption. Lemonade, a young company, is injecting new life into the sector with its AI-driven strategy. While the incumbents rely on AI for data analysis, Lemonade takes it a step further. By leveraging AI chatbots, the company communicates with customers and processes claims swiftly. In a world where time is money, Lemonade’s bots can settle claims in mere minutes, a stark contrast to the prolonged waits typically associated with traditional insurance companies.

Lemonade’s app-centric approach has attracted a growing customer base. With a 12% year-over-year increase in customer count to over 2 million, it’s evident that some customers are gravitating towards Lemonade from other providers. While its product offerings may not match those of its more established competitors yet, Lemonade provides a range of insurance policies, including renters, homeowners, car, pet, and life insurance.

Lemonade’s Path to Profitability

Profitability is the holy grail for insurance companies, and Lemonade is steadily progressing on that front. Although the company is not yet profitable, its non-GAAP EBITDA losses in Q4 shrank by 44% compared to the previous year. With $945 million in cash reserves and positive cash flow in the latter part of last year, Lemonade exhibits financial resilience.

Investing in Lemonade carries inherent risk, as the company navigates its journey towards profitability while expanding its customer base. However, with a market capitalization of $1.2 billion, Lemonade has the potential to revolutionize the insurance landscape if it establishes itself as a key player.

Opportunities for Investors

For investors seeking growth potential, Lemonade presents a compelling opportunity. As organizations increasingly prioritize cybersecurity measures, the demand for robust insurance coverage is on the rise. Lemonade’s combination of escalating free cash flow, a transition towards profitability, and alignment with a secular growth trend makes it a stock worthy of consideration.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.