Entering the Magical Kingdom of Stocks

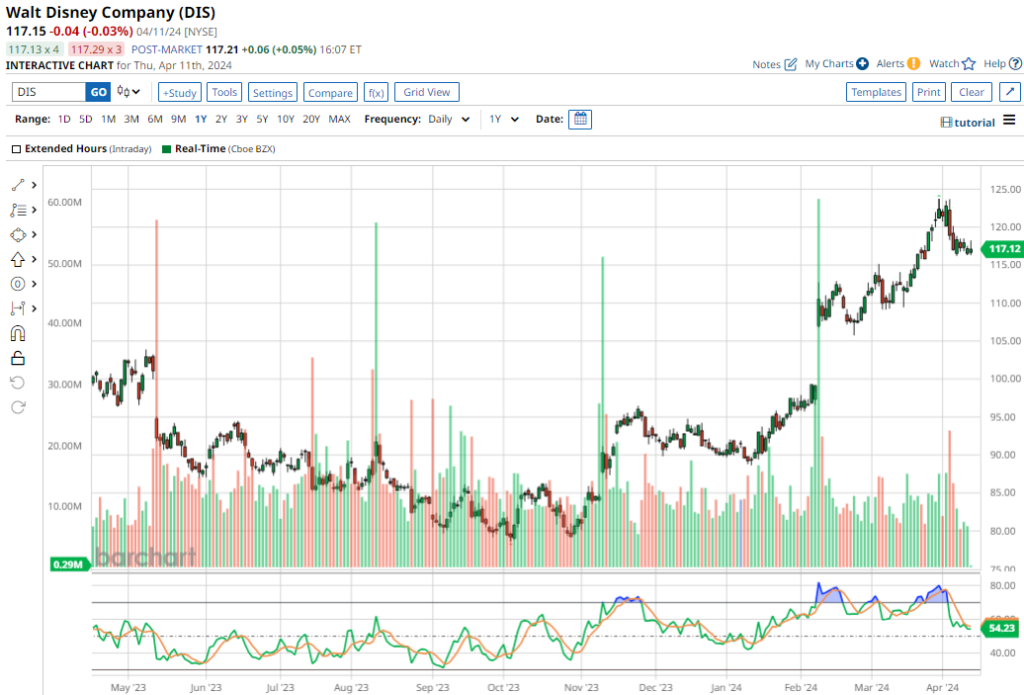

The Dow Jones Industrial Average ($DOWI) kicked off the year on a high note, with a 5.6% gain in the first quarter. Leading the charge was entertainment behemoth Walt Disney Company (DIS), boasting a stellar 34.9% return, clinching the title of the best-performing stock among all 30 Dow components.

Analysts at Bank of America (BAC) reiterated their “Buy” rating on Walt Disney stock in April, escalating the price target to $145. The focus was on Disney’s thriving park performance, hinting at a potential growth in overall operating income in the upcoming quarter.

Moreover, Disney emerged victorious in the costliest proxy battle in U.S. history, rebuffing activist investor Nelson Peltz’s push for a board seat. This win bolstered shareholder confidence, driving Disney shares to a nearly 26% increase post the proxy announcement.

Unpacking Walt Disney Stock

Based in Burbank, California, The Walt Disney Company (DIS) is a global brand powerhouse with a robust competitive edge. Leveraging its unparalleled storytelling prowess, Disney has diversified across various sectors. With a current market cap of $214.9 billion, Disney is making waves in the streaming wars, challenging industry stalwarts like Netflix (NFLX) and Amazon (AMZN) Prime Video.

While Disney weathered 2023 without recording losses, it lagged behind both the broader Dow Jones and the S&P 500 Index. Long term performance has trailed the Dow Jones over the past decade. Nonetheless, Disney shares have surged by nearly 17% in the past 52 weeks, outstripping the Dow’s 14.4% increase over the same period.

The reinstatement of dividends last year marked a turning point for Disney, with a recent 50% semi-annual dividend raise to $0.45 per share, translating to a yield of 0.77%. Trading at 2.43 times sales, Disney stands as a more economical option compared to its smaller rival, Endeavor Group (EDR), and substantially lower than Netflix (NFLX).

Disney’s Earnings Enchantment

In its fiscal Q1 earnings release, Walt Disney’s revenue inched up to $23.6 billion year-over-year, slightly missing consensus estimates. However, its adjusted EPS of $1.22 exceeded analyst expectations by 25.8%, buoyed by robust revenue growth in its theme parks sector and cost-saving measures.

The experiences segment revenue soared by 7% annually to $9.1 billion in Q1, with operating income climbing 8% to $3.1 billion. CEO Iger’s strategic cost-saving initiatives are yielding significant results, with the company poised to surpass the targeted $7.5 billion reduction in costs by September.

For fiscal 2024, Disney anticipates a minimum 20% EPS uptick to $4.60 and expects to generate approximately $8 billion in free cash flow. Analysts’ forecast a profit of $4.66 per share in fiscal 2024, a 23.9% increase year-over-year, with continued growth to $5.57 per share in fiscal 2025.

Crystal Ball: Analyst Predictions for Disney Stock

With an overall consensus of “Moderate Buy,” out of the 24 analysts tracking the stock, 15 stand by “Strong Buy,” four advocate for a “Moderate Buy,” four suggest “Hold,” and one weighs in with a “Strong Sell.” The average analyst price target for Walt Disney stands at $124.33, indicating a 6.1% potential upside.

The Street-high price target of $145, shared by Needham & Company and Bank of America Securities, implies a 23.7% rally from present levels, painting the picture of a potentially lucrative investment opportunity in the land of Disney.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.