One of the most disappointing international stocks over the past five years undoubtedly has been Chinese e-commerce, logistics, and technology infrastructure company Alibaba (NYSE: BABA). While the S&P 500 has risen over 80% over that time, Alibaba stock is down nearly 60%.

Over that period, Alibaba has been able to grow both revenue and earnings. For its most recent quarter, ended December 2023, the company reported revenue of $36.7 billion and adjusted earnings per American depository share (ADS) of $2.67. That’s decidedly better than its December 2018 quarter, when it recorded revenue of $17.1 billion and earnings per share (EPS) of $1.77.

Below, I’ll explore the factors contributing to the stock’s downturn and project its potential trajectory over the next five years.

Challenges Leading to Stock Decline

Part of Alibaba’s underperformance during the last five years can be tied to the poor performance of the overall Chinese stock market during that period. The S&P China 500 is down about 24% over the past five years. During this period, COVID-related lockdowns impacted China longer than many other countries, which has had a lasting impact on its economy.

Meanwhile, the Chinese government also began cracking down on Chinese tech firms during this time. In 2021, the government fined Alibaba over $2.5 billion for being a monopoly, while last year, it fined Alibaba’s affiliate Ant Group nearly $1 billion for breaking banking regulations. Meanwhile, company founder Jack Ma retired in 2019 and left public life for a few years after criticizing the Chinese government in 2020.

Overall, a weak Chinese stock market, slowing growth, government regulations, and the loss of the company’s well-respected founder have helped push Alibaba stock lower.

Undervaluation and Potential Strategic Moves

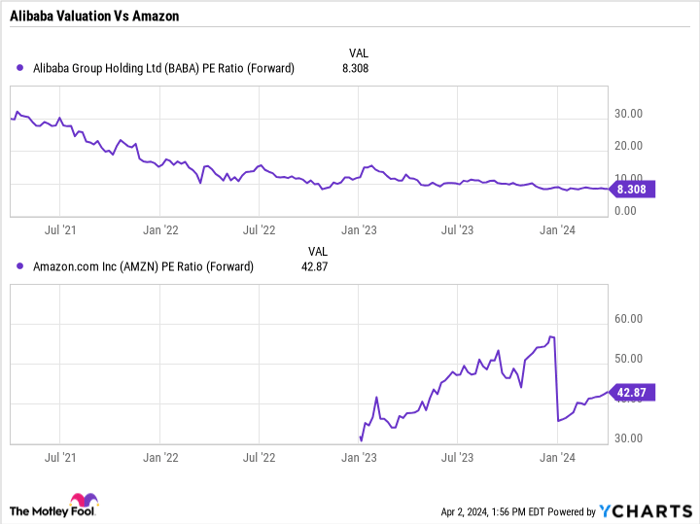

With a forward price-to-earnings ratio (P/E) of just over 8, Alibaba is a value stock at this point. It has often been called the Amazon of China, given their similar businesses, but the valuation gap between the two is substantial. Amazon is trading at nearly 43 times its forward P/E. Chinese-specific risks play a large part in the valuation difference between the stocks, but it wasn’t that long ago when Alibaba traded at a forward P/E in the 20 to 30 range.

BABA PE Ratio (Forward) data by YCharts.

One big thing to look at with Alibaba is its cash position and free-cash-flow generation. At the end of 2023, it had $68.6 billion in net cash while it was generating free cash flow of about $25 billion a year. Over the next five years, the company’s cash-flow generation and current net cash could be worth more than Alibaba’s current $176 billion market capitalization.

Alibaba has also discussed splitting the company into six separate businesses that would be run by separate CEOs and pursue initial public offerings (IPOs) and separate financing. So far, this plan has been delayed.

The company stated that market conditions would not be reflective of the intrinsic value of the businesses, such as its superstore Hema or its Cainiao logistics business. Last November, meanwhile, the company scrapped plans to IPO its cloud business because of U.S. export bans on artificial-intelligence (AI) chips going to China.

Image source: Getty Images

Future Outlook for Alibaba

Given Alibaba’s cash on hand and cash-flow generation, it would be surprising if the company wasn’t trading at a much higher price in five years. There’s also a good chance that it will be restructured as a holding company with a number of publicly traded individual businesses. This should unlock value for shareholders, as the individual businesses would likely be able to command higher valuation multiplies because each business would be valued on its own individual growth prospects.

The Chinese economy, meanwhile, is showing signs of stabilizing, with the manufacturing sector recently returning to growth after five months of declines. An improving Chinese economy should go a long way in helping a variety of Alibaba’s consumer-facing and logistics businesses.

At the same time, Alibaba won’t sit still and will invest in AI technology to improve its business operations. The company won’t get the same benefits as U.S. companies with access to powerful graphics processing units because of the U.S. export curb, but it still should be able to make progress on this front.

Given this backdrop, Alibaba should be a solid investment over the next five years. That said, there are certainly geopolitical and country-specific risks that need to be taken into consideration. Any tensions between the U.S. and China could negatively impact the company’s stock.

Considerations for Potential Investors

Before you buy stock in Alibaba Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alibaba Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 4, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Geoffrey Seiler has positions in Alibaba Group. The Motley Fool has positions in and recommends Amazon. The Motley Fool recommends Alibaba Group. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.