As the artificial intelligence (AI) revolution rolls on like a juggernaut, the “Magnificent 7” cohort of Microsoft (MSFT), Nvidia (NVDA), Amazon (AMZN), Google (GOOG), Tesla (TSLA), Apple (AAPL) and Meta Platforms (META) has been one of the main drivers of the stock market’s advance. With their seemingly bottomless resources, innovative edge, and enviable brand value, these seven companies have made huge strides in the tech industry.

In fact, the Roundhill Magnificent Seven ETF (MAGS) – an exchange-traded fund (ETF) designed to track the performance of these seven companies – is up nearly 58% since last April, crushing the returns of the broader equities market. However, as the performance of this group starts to diverge in 2024 – with names like Apple and Tesla both in the red – it’s worth noting that one Mag 7 member just scored a bullish note from Wells Fargo. Here’s a closer look at the brokerage firm’s upbeat forecast for Meta.

Wells Fargo Hikes Meta Price Target

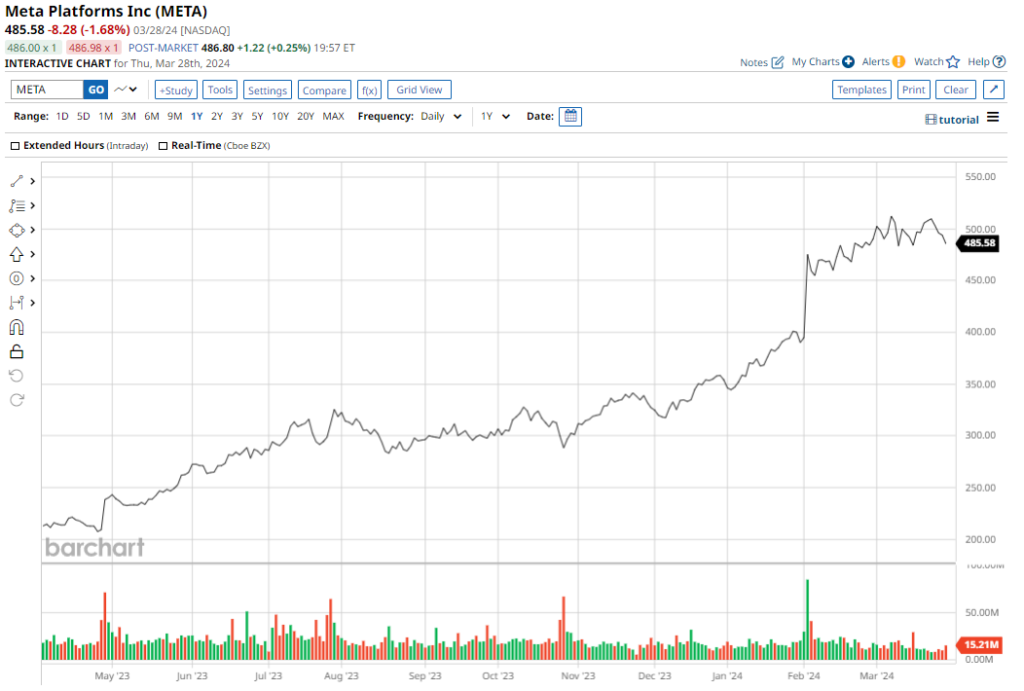

Wells Fargo analyst Ken Gawrelski recently reiterated a “Buy” rating on Meta and raised the stock’s price target from $536 to $609 – which implies an upside potential of about 24.2% from current levels. This expected upside is in addition to a 131.2% rise in the share price over the past year.

However, as with many other FAANG giants, the path higher for Meta stock could be riddled with regulatory potholes. With the new digital law in place in Europe, and U.S. regulators still targeting Big Tech, it might not be smooth sailing for META going forward.

So, why is Wells Fargo raising the stakes on Meta now? Let’s try and find out.

TikTok Ban: One potential upside catalyst for Meta stock would be a proposed ban of Chinese-owned short video company TikTok. After the House passed legislation that would allow TikTok to operate in the U.S. only if its Chinese owner, ByteDance, sells its stake in the company, market veterans have argued that Meta’s Instagram Reels is poised to be a natural beneficiary.

With more than 170 million American users on its platform, a ban on TikTok could lead to massive content creator migration to Meta’s social media platforms, especially Reels – which now makes up one-third of the video viewing time spent on Facebook, up 70% year-over-year. With Meta’s AI-fueled algorithm, a combination of personalized social discovery and advertising is expected to be a major driver of growth.

Also, Meta’s Threads app could get a new lease on life from increased user engagement, considering that the hype surrounding its breakout debut, when it reached 100 million users within the first week, has died down considerably.

Strong Quarterly Results: Meta’s latest results for the fourth quarter featured a beat on both revenue and earnings. Revenues for the quarter came in at $40.1 billion, up 25% from the previous year, while EPS more than tripled to $5.33. Looking back, Meta’s EPS have topped expectations in 4 out of the past 5 quarters.

The social media giant also reported a 6% yearly rise in daily active users (DAUs) to 2.11 billion, on average, for December 2023. On the liquidity front, Meta exited the quarter with a cash and equivalents balance of $65.4 billion, much higher than its long-term debt levels of $18.4 billion.

And one key highlight of the results was the initiation of a quarterly dividend for Meta shareholders. The quarterly dividend of $0.50 per share is the company’s first, and it intends to pay dividends on a quarterly basis, subject to market conditions.

With its robust balance sheet, operational strength, and now a quarterly dividend, the company remains well-poised to attract investors.

AI Boost: Meta is also strengthening its AI capabilities, keeping WhatsApp Business at the forefront. With WhatsApp Business’ AI capacities, assistants can eventually automatically answer customer questions, and perhaps even automate sales in the future.

Further, to reduce its computational costs and improve its models, Meta is establishing its large language model Llama as an open-source standard.

Lastly, in the realm of generative AI, Meta fully rolled out its AI assistant and other AI chat experiences in the U.S. at the end of the year and began testing more than 20 GenAI features across its Family of Apps.

Industry-Beating Growth Forecasts: Broadly speaking, most analysts are expecting Meta to report strong growth that will surpass the rest of the tech sector. Forward revenue growth is projected at 15.2%, versus the median sector estimate of 3.04% by a wide margin.

Likewise, META is expected to notch operating profit growth of 34.51% (vs. 5.18% for the broader tech sector) and forward EPS growth of 39.21% (vs. a sector median of 5.29%).

Analyst Optimism: “Optimism,” quite simply, is the best way to describe the attitude of the wider analyst community about Meta stock. Overall, analysts have a consensus rating of “Strong Buy” for Meta. Out of 44 analysts covering the stock, 39 have a “Strong Buy” rating, 1 has a “Moderate Buy” rating, 3 have a “Hold” rating, and 1 has a “Strong Sell” rating.

The mean price target is $502.80 – which denotes an upside potential of roughly 2.5% from current levels. That means Wells Fargo has a significantly higher forecast than the consensus, and suggests we could see more price-target hikes coming down the pike for META stock soon from this bullish group.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.