The “Magnificent Seven” has been the driving force behind the market’s upswing since the dawn of 2023. Yet, these stalwart stocks are now revealing chinks in their once-impenetrable armor. Some have soared too high, perched atop lofty valuations that defy gravity, despite commendable business performance. But is the entirety of the cohort teetering on the brink of overvaluation?

Changes in Dominance for the Magnificent Seven

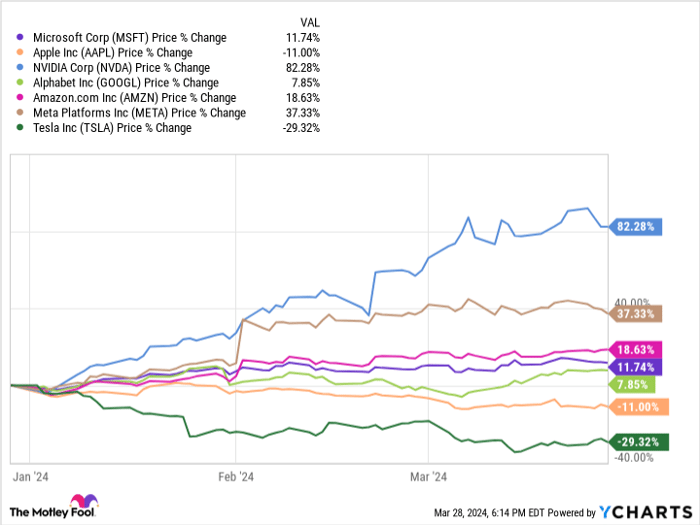

Comprised of Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta Platforms, and Tesla, the Magnificent Seven witnessed a phenomenal surge in 2023. However, the dynamics have shifted in 2024, scattering their performances far and wide.

A tumultuous tide in valuation has surged, prompting investors to hesitate before paying the premium to acquire these stocks. As growth-centric enterprises, assessing their worth entails a keen consideration of revenue amplification and forward price-to-earnings (P/E) ratios, two yardsticks that offer a broader canvas of valuation.

Tesla, facing a turbulent year, has shed nearly a third of its market cap, as slowing electric vehicle sales and intensifying competition gnaw at its margins. The once-inflated premium that investors gladly shelled out now stands at 55 times the anticipated earnings.

Apple finds itself ensnared in a similar narrative, grappling with prolonged growth stagnation. Despite current valuations pegged at 26 times forward earnings, the tech titan’s growth trajectory fails to justify its premium price tag.

While 2024 has been a mixed bag for the Magnificent Seven, not all are cast in the same overvalued mold.

Divergent Trajectories of the Remaining Five

Alphabet and Meta Platforms emerge as the unsullied beacons of modest valuation within the hallowed circle. Nestled at 22 times forward earnings, Alphabet, notwithstanding the PR hurdles stemming from its generative AI model, boasts the most palatable price tag amongst its peers.

Meta Platforms, harmonizing closely with Alphabet’s trajectory, trades at a modest 25.5 times forward earnings, propelled by its robust foothold in the advertising realm across diverse social media platforms.

Nvidia, the harbinger of an unfolding AI revolution, resonates with tremendous growth potential, encapsulated by an ambitious forward earnings multiple of 38 times.

Amazon’s valuation conundrum hinges on a profit optimization journey that renders its forward earnings multiple askew. Anchored at 42 times earnings, the e-commerce behemoth awaits a future where its burgeoning gross profit margins shall unfurl a more compelling narrative.

Microsoft, despite commanding the pinnacle of market capitalization, finds itself saddled with a hefty valuation, perched at 37 times forward earnings. A formidable contender in AI innovations and cloud computing, Microsoft’s frothy valuation belies its growth rate and profit optimization.

In the grand scheme of things, these valuation dynamics throw down the gauntlet: how do these stocks merit placement from the cheapest to the most expensive?

Assessing Value Amidst Fluctuating Realities

Ranking the ensemble by the forward price-to-earnings (P/E) metric alone might paint an incomplete picture—while Apple grapples with growth headwinds, Nvidia revels in tripled revenue streams. These rankings waltz beyond mere metrics, embracing nuances of present growth trajectories and future vistas.

Here’s my rendition of the Magnificent Seven, from the modestly priced to the dear ones:

- Alphabet

- Meta Platforms

- Amazon

- Nvidia

- Tesla

- Microsoft

- Apple

Crowning Alphabet and Meta Platforms with the laurel of affordability was a foregone conclusion. Amazon and Nvidia hold promise for extended growth trajectories, making their lavish valuations appear a tad more reasonable. As for Tesla, navigating its future amid a potential EV surge remains a puzzle. Microsoft, the venerated giant, embraces a premium valuation, underscoring its growth and profit optimization saga.

Unearthing the Truth Behind Pricy Growth Stocks

The High Cost of Growth

When it comes to evaluating pricey growth stocks, it seems that both Amazon and Apple are leading the pack, with Apple taking the title of the top offender due to its sluggish growth rate.

Investors must dissect the numbers and charts to determine whether any of these stocks are trading at a bargain that warrants a purchase.

Insights on Nvidia Investment

Is investing $1,000 in Nvidia the right move at this juncture? Before making a decision, it’s imperative to contemplate the following:

The analyst team at Motley Fool Stock Advisor recently uncovered what they believe to be the ten most lucrative stocks to invest in at the moment, and Nvidia did not make the cut.

These selected stocks are projected to yield substantial returns in the foreseeable future, diverging from Nvidia’s potential.

The Power of Stock Advisor

Stock Advisor from Motley Fool offers a comprehensive roadmap to financial success for investors. This includes tailored advice on constructing a well-diversified portfolio, frequent updates from analysts, and two fresh stock recommendations each month.

Since 2002, the Stock Advisor service has significantly outperformed the S&P 500, tripling its return and showcasing the prowess of their investment strategies.

This service arms investors with the right tools and insights to navigate the complexities of the stock market successfully.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.