Credit Card Delinquencies Show Modest Decline, Net Charge-offs Rise in February

Kenishirotie/iStock via Getty Images

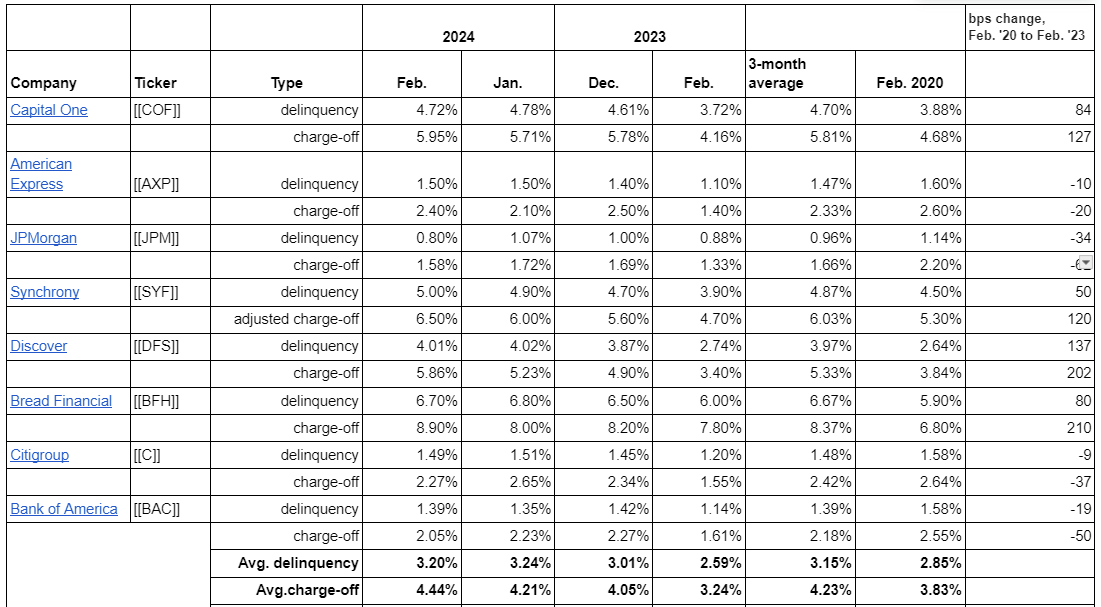

Credit card lenders witnessed a slight decrease in delinquencies in February, while net charge-offs continued on an upward trajectory according to data compiled by Seeking Alpha.

The average delinquency rate of 3.20% showed a marginal increase from 3.24% in January and 2.59% in February 2023.

The current figure has crept slightly above the 2.85% mark noted in February 2020 amidst the onset of the pandemic-triggered economic turmoil. Notably, at major players such as American Express, JPMorgan Chase, Citigroup, and Bank of America, delinquency rates stand below pre-pandemic levels from February 2020.

In contrast, the average net charge-off rate of 4.44% rose from 4.21% in January and 3.24% in February 2023. This is a significant uptick from the 3.83% seen back in February 2020.

John Hecht, an analyst at Jefferies, highlighted that the seasonal dip in credit card delinquencies during February was weaker than usual, while net charge-offs saw a more pronounced increase.

Hecht remarked, “The year-on-year percentage change in delinquencies improved by -9 basis points compared to the previous month, a crucial trend that must continue gaining momentum in the coming months for the anticipated peak in the net charge-off cycle to materialize in the second half of 2024 — a milestone currently under consideration by many.”

Loan balances at institutions covered by Hecht experienced a 1.4% month-on-month decline to $480 billion, aligning with historical trends for February and reflecting a 10% year-on-year increase. “Given the prevailing macroeconomic conditions, issuers have tightened credit standards, and as a result, loan growth in ’24 is projected to be much weaker,” he noted.

Hecht further highlighted, “Monthly payment rates also indicate a deceleration in loan growth going forward.”

“Payment rates serve as a leading indicator for loan growth trends, hence considerable attention will be directed towards monitoring this metric closely,” Hecht conveyed. “We anticipate persistently high prepayment rates throughout ’24 leading to a slowdown in loan growth.”

Further Insights into Industry Trends

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.