The Contrasting Trajectories of UiPath and Unity Software Stocks

Artificial intelligence (AI) stocks have maintained their appeal in 2024, with investors showing unwavering optimism towards the AI wave poised to attract billions in investments in the coming decade. While heavyweight players like Nvidia (NVDA), Microsoft (MSFT), and Alphabet (GOOGL) dominate the headlines, there are lesser-known AI stocks like UiPath (PATH) and Unity Software (U) that are silently positioning themselves to offer substantial returns for investors in 2024 and beyond.

The Case for UiPath Stock

UiPath (PATH) provides an enterprise-focused platform for automating business processes across industries such as healthcare, telecom, finance, and banking.

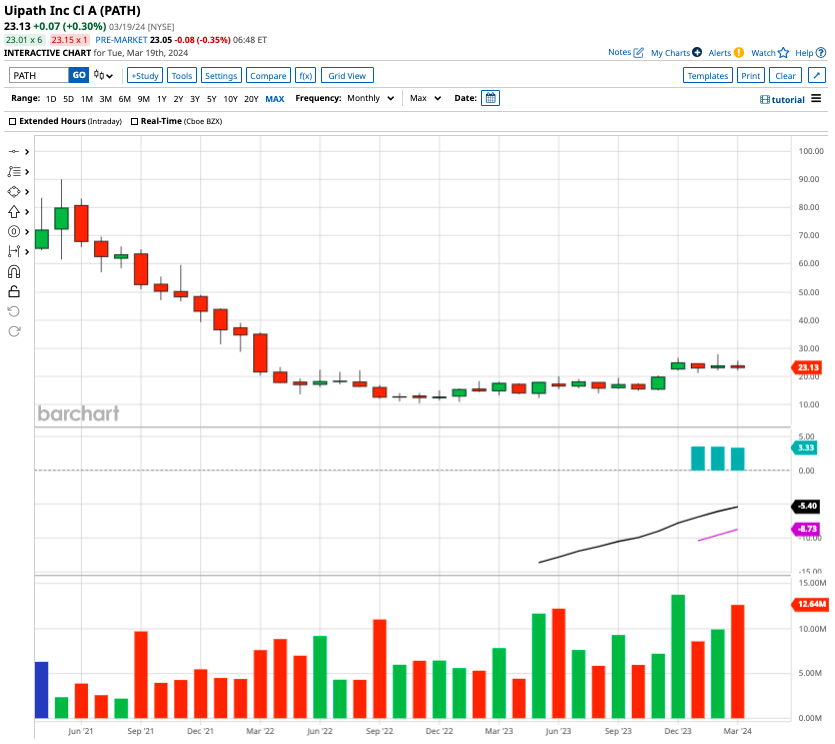

With a market capitalization of $13 billion, UiPath’s stock currently trades at a significant discount of 74.5% from its peak. Despite this, buoyed by the positive sentiment towards AI stocks, PATH has seen a 35% surge in the past six months.

A major player in robotic process automation (RPA), UiPath offers automation solutions for functions like accounts payable, claims processing, and finance. Grand View Research predicts the RPA market to reach $30 billion by 2030, leaving UiPath ample room for growth, having raked in $1.31 billion in revenue for fiscal 2024 (ending in January). If UiPath maintains its market share, it could potentially hit the $14 billion revenue mark by fiscal 2030.

In stark contrast to many AI growth stocks, UiPath consistently turns a profit. In fiscal Q4 of 2024, it reported adjusted earnings of $0.22 per share, surpassing estimates of $0.16 per share. The company’s revenue stood at $405 million, outperforming estimates by $21 million and representing a 31% year-over-year increase. For fiscal 2025, UiPath anticipates sales of $1.56 billion with adjusted free cash flow hitting $350 million, translating to a 22% margin.

Of the 18 analysts covering UiPath stock, seven advocate a “strong buy,” one suggests a “moderate buy,” and 10 recommend a “hold.” The average target price sits at $25.71, pointing towards an 11.1% upside potential from current levels.

Assessing the Viability of Unity Software Stock

Unity Software (U) boasts a market capitalization of $10 billion but currently finds itself at a downtrend of 87% from its peak in March 2021. Specializing in video gaming software, Unity offers solutions to develop, manage, and monetize interactive content for various platforms including smartphones, tablets, consoles, and augmented or virtual reality devices.

In Q4 of 2023, Unity reported revenue of $451 million, trumping estimates of $395 million. Despite this, the company’s losses narrowed to $254 million, equivalent to $0.66 per share, compared to $299 million in the preceding year. However, analysts had anticipated a narrower loss of $0.45 per share in Q4.

Facing a slowdown in revenue growth amidst a challenging economic backdrop, Unity managed to reduce its cost structure over the last 12 months. This strategic move led to a loss of $826 million in 2023, down from a net loss of $921 million in 2022.

Unity’s adjusted EBITDA margin in Q4 of 2023 stood at 30%, a substantial leap from 5% in the previous year. While the company is narrowing its losses, analysts predict a 16.8% decline in sales for Unity Software, amounting to $1.82 billion in 2024.

Among the 19 analysts monitoring Unity stock, six issue a “strong buy” recommendation, one suggests a “moderate buy,” 10 opt for a “hold,” and two propose a “sell.” The average target price for Unity stock is $30.83, implying a 17% upside potential from current levels.

While analysts project Unity to offer greater upwards momentum compared to UiPath at present, investors should approach with caution given Unity’s notable earnings miss, which has seen its shares recede approximately 20% from their pre-earnings levels above $33.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.