The landscape of the electric vehicle (EV) industry in 2024 resembles a tumultuous battleground; a clash of optimism and skepticism where even the giant Tesla (TSLA) faces the heat. Emerging from a haze of supply chain woes, the industry grapples with a new adversary – swooning consumer interest. The ongoing EV price war mercilessly crushes profit margins across the sector, pushing some EV startups into the abyss of bankruptcy.

For Tesla, the path forward appears shrouded in clouds. Disappointment looms large among investors and analysts alike. The company’s projection of tepid volume growth and uncertainty surrounding the launch of a new model, crucial for propelling future growth, has failed to ignite much excitement. A shadow crawls over the house of Tesla as its birthplace rival, BYD (BYDDY), gains ground, particularly on the Chinese mainland, amidst a cooling local economy.

Adding salt to the wound are the flamboyant antics of CEO Elon Musk, alongside a recent unfortunate incident involving suspected arson at a Tesla plant in Germany. Tesla’s revered status as a “Magnificent 7” stock has faded, relegating it to an outcast among other mega-cap leaders on Wall Street.

Let’s dissect the current state of TSLA shares and unpack the speculation among industry pundits.

The Unraveling of Tesla Stock

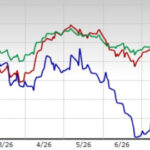

In stark contrast to the broader market’s upward trajectory, Tesla (TSLA) has witnessed a stark downturn in 2024. After a stellar performance in 2023, the stock now languishes at a 34.2% plummet year-to-date, ranking as the worst performer in the S&P 500 Index for 2024. This decline translates to a market cap erosion of approximately $269 billion – a figure equivalent to the entire market value of Netflix (NFLX).

Yet, amidst the chaos, a glimmer of hope emerges. TSLA shares currently stand as a bargain by certain measures. Priced at 4.72 times forward earnings, the stock presents nearly a 50% discount compared to its historical norms. However, it still commands a significant premium over competitors like Toyota Motor (TM), trading at 1.05x sales, poised to capitalize on a rising trend toward hybrid vehicles over fully electric models.

The ongoing debate rages on whether Tesla’s valuation warrants a recalibration, possibly aligning its tech-oriented premiums more closely with traditional auto industry metrics. Musk’s recent hints about tying progress in artificial intelligence (AI) and robotics at Tesla to his voting stake size only add to the conjecture.

Moreover, analysts have begun to revise their outlook on TSLA, with some delivering rather harsh critiques.

Future Projections for TSLA Stock

Last week, Wells Fargo’s analyst Colin Langan dealt a blow to Tesla stock, downgrading it from “equal weight” to “underweight” and revising the price target downward to $125 per share from $200. This revision anticipates a 23.5% downside from Friday’s closing price. Langan attributed this move to the risk of dwindling volume due to price reductions and headwinds from disappointing deliveries, factors likely to drive negative earnings per share (EPS) revisions.

Another striking opinion emanated from Evercore analyst Chris McNally, who painted Tesla as a “2027 story,” candidly hinting at a delayed narrative after a factory tour stirred doubts.

Tesla’s Bumpy Ride: Analysts Divided on Future Growth Prospects

As analysts continue to quarrel over Tesla’s future growth trajectory, investors are left to navigate a bumpy road of conflicting opinions on the electric vehicle maker. On one side of the spectrum, the bearish camp, we have McNally, who rates TSLA a “hold.” This stance is echoed by Bernstein’s Toni Sacconaghi, who maintains a “sell” rating with a price target of $150 – underscoring a pessimistic outlook. Sacconaghi had previously prophesied a TSLA short as his best idea for 2024, with a call for a 40% downside over the next 12 months – a prediction that is not far off as Tesla stock hovers at a precarious 8.3% away from his forecast.

Bullish Sentiment: Analysts Defend Tesla’s Potential

Contrary to the bearish forecasts, some analysts like Dan Ives are waving the bull flag high. Ives, from Wedbush, believes that Tesla’s recent sell-off has been overblown and presents an enticing risk/reward scenario at current levels. In a bold statement, Ives predicts that the stock could soar to exceed a $1 trillion valuation as Tesla’s AI capabilities and full self-driving technology propel the company into a new era of growth. Ives maintains an “Outperform” rating on Tesla with a price target of $315, representing a premium of 92.6% from the previous closing price.

Analysts Split: Ambivalence in Consensus Rating

The tug-of-war between contrasting views is evident in the shifting consensus rating for Tesla, which has veered down to a “hold” from a “moderate buy” just two months ago. Despite this equivocation, the mean price target of $214.31 suggests a potential upside of about 31% from the recent closing price, painting a somewhat optimistic picture amidst the divergent opinions.

Investor Caution Advised Amidst Volatility

With Tesla priced at 37.58 times projected 2025 earnings and 3.92 times expected 2025 sales, some bargain-hunting investors may find the current valuation attractive. Nevertheless, the inherent volatility of Tesla shares underscores the importance of caution, suggesting that these stocks may be better suited for investors with a higher tolerance for risk and uncertainty.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.