The recent turbulent churn of the stock market seems akin to a storm-battered ship needing respite in a safe harbor. As Wall Street pauses to tally profits, there’s a gradual descent from the recent high-flying frenzy, with the Nasdaq, for instance, dipping under its loyal 21-day benchmark—a trendsetting level that had given robust backing throughout 2024.

The inevitable swerve towards longer-term averages like the 50-day or 21-week was always on the horizon. The coming deeper decline could knock on the door now or later, yet it must be seen as an opening for savvy investors.

While the specter of inflation and interest rates looms, the bullish sentiment lingers among investors, who are keen on staying engaged with the market this year. For those with a long-term perspective, the trajectory appears clear.

Stride, Inc. (LRN): The Academic Aviator

In the tumult of stock rises and falls, one standout is Stride, Inc., whose stock has surged by a staggering 110% in the past three years, galloping past the tepid 30% performance of its benchmark. An impressive 53% leap over the last 12 months outclassed the Zacks Tech sector’s commendable 47%.

As LRN spreads its wings, it isn’t merely a flash in the pandemic pan. Over the past decade, LRN has soared by 180%, mirroring the S&P 500’s stride. Despite a recent cooling off, Stride is marking time since early December, presenting a ripe opportunity for potential investors.

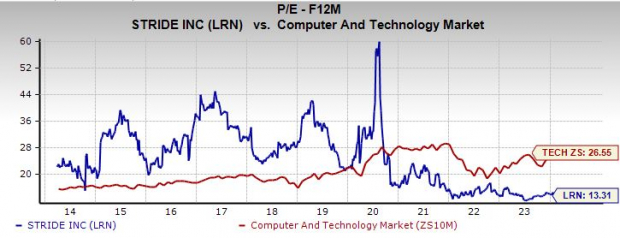

Down-to-earth metrics depict LRN finding support at its 21-week moving average. Although facing the imminent headwinds of market volatility, Stride still trades notably below its average Zacks price target, pitching itself as a bargain buy. The stock’s valuation also speaks volumes, with a staggering 80% discount to its peaks and a trading price 45% under its 10-year median, standing at 13.3X forward earnings—a clear case of an undervalued gem.

The allure of Stride lies in its digital educational offerings, casting a wide net across students of all ages, both in the U.S. and abroad. As LRN diversifies its portfolio to cater to various educational needs, the company’s growth trajectory seems boundless, especially in a landscape where digital education is gaining immense traction.

Toll Brothers, Inc. (TOL): The Luxurious Luminary

Another titan worthy of investor attention is Toll Brothers, Inc., a luxury homebuilding maestro. In a five-year span, TOL stock has ascended by an awe-inspiring 230%, outpacing the S&P 500 twofold and dwarfing the Zacks Construction sector’s modest 150% climb. Notching a notable 100% surge in the past year and a steady 16% year-to-date uptick, Toll Brothers shows no signs of resting on its laurels.

Although perched precariously atop Technical indicators as overbought on a 10-year timeline and far above its 21-day and 21-week moving averages, TOL remains a beacon of promise, even as it trades near historic highs.

A deeper scrutiny reveals that Toll Brothers is a cut above trading at a substantial 50% discount to the Construction sector and a notable 17% below the Home Builders industry metrics. With TOL’s trading price now sitting at a commendable 55% under its zenith over the last decade, it stakes a clear claim as an underpriced asset.

The bedrock of Toll Brothers’ success lies in its diversified operations spanning architectural, engineering, mortgage, and title services, enriched by a regional footprint that counts over 60 markets across half of U.S. states.

Despite the impending slackening in the housing market pace, Toll Brothers recently saw a surge in earnings revisions post-February 20, paving the way for a Zacks Rank #1 (Strong Buy). The net signed contract value for TOL shot up by an impressive 42% in Q1 FY24, highlighting a robust path ahead.

In an environment where Millennials steer the housing domain and Baby Boomers embrace retirement relocations, the long-term view for Toll Brothers gleams brightly. Unlike the overzealous building spree during the Covid era, the relative restraint of home builders like Toll Brothers has left a gaping demand-supply chasm which promises continued prosperity.

Murphy USA: Fueling Growth in the Gas Station Industry

Murphy USA, a dominant force in the gas station sector, has experienced a meteoric rise over the past decade. With MUSA stock soaring 930%, it has outshone the benchmark’s 180% surge, leaving the Oil and Energy industry’s 17% decline in its wake. Over the past three years, Murphy USA shares have climbed 220%, surpassing the sector’s 43% growth, driven by an impressive 70% increase in the last 12 months compared to Oil and Energy’s 13%.

The Meteoric Rise

Murphy USA rebounded above its 21-day moving average recently, setting course for new records. The stock, akin to the overall market, is poised to challenge its 21-week moving average in the near future. A glance at the chart reveals its consistent upward trajectory over the past decade.

Financial Resilience

From a value perspective, MUSA is currently trading at its 10-year median and stands 33% below its peak at 16.2 times forward 12-month earnings. Additionally, the company allocates funds to dividends and buybacks, enhancing shareholder value.

Operational Strength

Murphy USA operates a vast network of retail stations, strategically located near Walmart outlets predominantly in the Southeast, Southwest, and Midwest regions. Serving approximately 1.6 million customers daily, the company also boasts a dedicated line space on the Colonial Pipeline, the largest refined products system in the United States.

Positive Earnings Outlook

Murphy USA’s earnings outlook has consistently improved over the past five years, culminating in a Zacks Rank #1 (Strong Buy) following its post-Q4 earnings release, reflecting positive sentiment among analysts.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.