Sports betting stock DraftKings (NASDAQ: DKNG) has been soaring recently, with a staggering 140% surge over the past 12 months thanks to its expansion into new U.S. states. While this exuberant surge may give some potential investors pause, there are substantial reasons to consider diving into DraftKings’ stock now.

Despite anticipated volatility, the underlying upward momentum appears to be strong. Here are three compelling reasons to consider adding DraftKings to your portfolio.

1. Bright Future in Expanding Sports-Betting Market

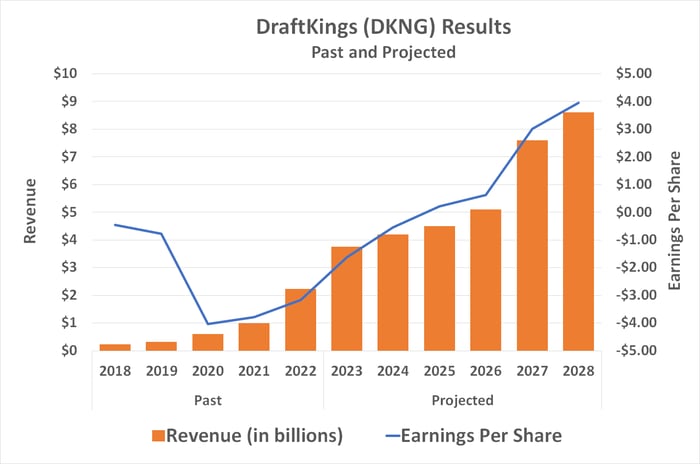

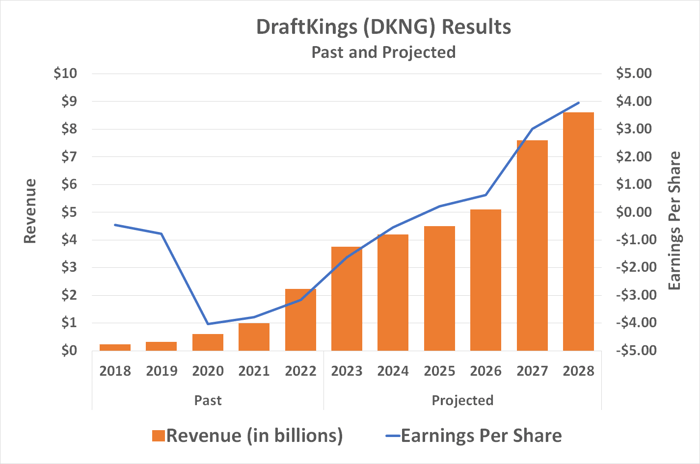

While much of DraftKings’ impressive 75% revenue growth in the first three quarters of last year can be attributed to organic expansion, the growing legalization of sports betting has played a significant role. Several states, including Kentucky, Pennsylvania, and Massachusetts, opened up to sports betting in 2023, bolstering DraftKings’ revenues.

However, significant potential remains untapped, with around 12 states and additional territories yet to legalize online sports betting, including the high-potential California market. Since the landmark U.S. Supreme Court ruling in 2018 striking down the nationwide ban on sports betting, most states have at least entertained legislation to allow it. This indicates a growth trajectory for the global sports betting market, with analysts forecasting annualized growth of over 11% through 2032.

Moreover, DraftKings has exhibited remarkable market share expansion, controlling 33% of the U.S. online sports betting and iGaming market as of the third quarter of last year, up from 25% a year earlier.

2. Path to Profitability

Despite operating in the red for the most part of its history, DraftKings is making significant strides toward profitability. The company managed to trim its total operating losses to $745 million in the first three quarters of 2023, a notable improvement from the $1.3 billion loss at the same time the year before. The anticipated first net profit, expected to be reported in mid-February, further underscores this progress.

Although the company is still anticipated to incur a full-year loss in 2024, analysts project a potential swing to profitability in 2025, with profit margins set to expand and outpace long-term revenue growth.

Data source: StockAnalysis.com. Chart by author.

Although actual earnings would undoubtedly bolster the case for DraftKings, the promising trajectory toward profitability is sufficient to attract investor attention.

3. Expanding Strategic Partnerships

While DraftKings initially relied on direct user acquisition, the company is increasingly focusing on strategic partnerships to drive growth. Collaborative initiatives, such as the planned sportsbook in Maine with the Passamaquoddy Native American tribe and the online casino gaming co-launched with the Golden Nugget in Pennsylvania, exemplify this strategy.

Moreover, the potential collaboration with Barstool Sports, although merely speculative at this stage, serves as a testament to DraftKings’ ability to forge impactful partnerships and capitalize on significant brand recognition.

Well-Suited for the Risk-Tolerant

Admittedly, DraftKings might not fit the bill for every investor, as it remains an aggressive growth pick with above-average risk. Those seeking safety, value, or income might find better alternatives elsewhere. However, investors with an appetite for volatility may find DraftKings’ potential upside to be worth the associated risk, albeit over a longer time horizon.

Reconsidering DraftKings Stock: A Contrarian View

Analyst Assessment

Before you buy stock in DraftKings, take a moment to consider a contrarian view. The Motley Fool Stock Advisor analyst team recently pinpointed what they believe are the top 10 stocks for investors to buy now, and DraftKings didn’t make the cut. While this may raise some eyebrows, it’s essential to recognize that the stock market is a complex and dynamic arena where consensus does not always guarantee success.

Stock Advisor provides investors with a roadmap for success, offering guidance on portfolio construction, regular analyst updates, and two new stock picks each month. Notably, the Stock Advisor service has significantly outperformed the S&P 500 since 2002*, reflecting the value of embracing a contrarian perspective.

Alternative Considerations

While conventional wisdom may sway investors towards the stocks in favor, it is crucial to remember the words of famed investor Warren Buffett, “Be fearful when others are greedy and greedy when others are fearful.” Such contrarian wisdom pertains to DraftKings stock. The act of contrarian investing is predicated on the belief that the consensus may be wrong. Therefore, investors should carefully evaluate DraftKings’ potential with a critical eye, unwilling to be entirely swayed by majority opinion.

Critical Evaluation

Seeking out perspectives that challenge prevailing opinions is crucial in navigating the financial markets. Numerous instances in history have illustrated the perils of blind conformity to popular sentiment. In fact, legendary investor Sir John Templeton brilliantly asserted, “Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.” These words remind us that contrarian thought is, at its core, a prudential—and often profitable—way of thinking.

Final Thoughts

In conclusion, the omission of DraftKings from the list of recommended stocks may, in fact, offer a unique opportunity. Investors should absorb the contrarian perspective presented by the Motley Fool Stock Advisor, critically evaluating the potential of DraftKings stock without succumbing to the allure of popular opinion. As with any investment, independent research, prudence, and a willingness to swim against the current are essential ingredients in the pursuit of financial success.

*Stock Advisor returns as of January 29, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool recommends the following options: long January 2025 $25 calls on Penn Entertainment and short January 2025 $30 calls on Penn Entertainment. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.