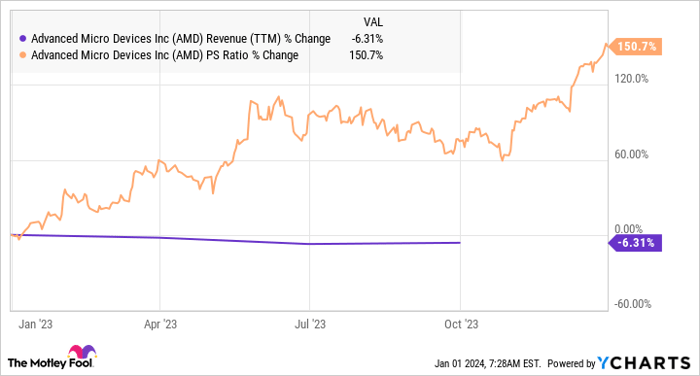

Advanced Micro Devices(NASDAQ: AMD) has experienced a remarkable rally over the past year, with its stock surging 127% despite a recent contraction in revenue and earnings due to a slump in the personal computer market. This might give prospective investors pause, questioning the wisdom of investing in AMD given its inflated valuation.

However, discerning investors should look beyond these recent setbacks. There are compelling reasons to believe that AMD is on the cusp of a significant resurgence, driven by two major catalysts with the potential to propel the company forward in 2024 and beyond.

A PC Market Rebound

AMD’s underperformance in 2023 was primarily attributed to the decline in PC sales. Yet, 2024 holds promise as industry experts project an 8% uptick in PC sales following a 12.4% dip in 2023. This uptick will significantly benefit AMD’s client CPU business, which heavily relies on PC sales. Consequently, the anticipated revival in demand is expected to reinvigorate AMD’s client revenue, a segment that accounted for 19% of its total revenue in the first three quarters of 2023.

Notably, the same segment saw a remarkable recovery in Q3: a 42% year-over-year increase in client revenue. This turnaround sets the stage for AMD’s ascent from its recent predicament.

AI and Revenue Potential

Besides the PC market rebound, another significant growth driver for AMD is their burgeoning pipeline of customers for their AI chips. Major players like Meta Platforms, OpenAI, Oracle, and Microsoft have committed to deploying AMD’s flagship MI300X AI accelerators. AMD forecasts its AI chips to generate at least $2 billion in revenue in 2024, potentially exceeding current expectations.

Furthermore, the company’s data center GPU business is expected to generate $400 million in Q4 revenue, hinting at a potential surge in quarterly revenue run-rate to $500 million, outstripping their prior estimates.

If AMD manages to secure a sizeable share of the AI chip supply from its foundry partner, the company could experience even greater growth in the data center GPU business. Notably, industry sources project a shipment of 400,000 AI GPUs in 2024, hinting at a significant potential revenue of $12 billion from this segment alone.

Favorable Trends Ahead

Looking forward, AMD’s prospects are highly promising. The company’s revenue and earnings are set to revert to strong growth in 2024, followed by another robust year in 2025. As affirmed by the following table, a bullish outlook is evident:

Year | Revenue estimate (in $billion) | Year-over-year change (%) | Earnings per share estimate | Year-over-year change (%) |

|---|---|---|---|---|

2023 | $22.7 | -4% | $2.65 | -24% |

2024 | $26.5 | 17% | $3.83 | 45% |

2025 | $31 | 17% | $5.16 | 35% |

Source: YCharts and Yahoo! Finance

Forthcoming earnings and sales multiples for AMD appear more attractive compared to earlier trailing multiples. The market is poised to reward the acceleration in AMD’s growth, especially given the expansive potential in the AI chip market. As such, shrewd investors seeking to capitalize on the accelerating adoption of AI and the resurgence of the PC market should mull over adding AMD to their portfolios before it takes flight.

Is Advanced Micro Devices a Good Investment?

Analyst Perspective on Advanced Micro Devices Investment

Before rushing into the prospect of acquiring Advanced Micro Devices stocks holds in investment portfolios, investors are advised to weigh crucial insights:

The Motley Fool Stock Advisor analyst team has disclosed a selection of what they consider as the most promising stocks for investors to allocate funds in, with Advanced Micro Devices not being one of them. The stocks highlighted are potentially positioned to deliver substantial yields in the years ahead.

For investors seeking a clear roadmap to prosperity, the Stock Advisor provides comprehensive support, offering guidance on crafting a formidable investment portfolio, periodic inputs from analysts, and two new stock recommendations monthly. Since 2002*, the Stock Advisor service has significantly outperformed the S&P 500 by tripling its return.

Investors can look up these elite ten stocks to understand the possible grounds for their exclusion.

*Stock Advisor’s returns are accurate as of December 18, 2023

Randi Zuckerberg, the former director of market development and spokesperson for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no stock positions in any of the companies mentioned. The Motley Fool holds positions in and recommends Advanced Micro Devices, Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Fool strictly adheres to a comprehensive disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.