Apple (NASDAQ: AAPL) stock is coming out of a solid growth year, with its shares climbing 48% in 2023. However, the company’s stock performance doesn’t tell the whole story.

Macroeconomic headwinds caught up with Apple last year, causing reductions in consumer spending and repeated declines in product sales. Meanwhile, the company had to contend with restrictions on its smartphones in China and a potential patent infringement with its new Apple Watch. The issues culminated in a 3% year over year decline in revenue for the company’s fiscal 2023.

However, Apple remains a tech behemoth with vast financial resources. Its reputation saw investors stick with the company even through challenging market conditions last year, illustrated by its stock growth. The company is in a slump, but it’s unlikely to last forever.

Here’s why it’s not too late to buy Apple stock — but be prepared to hold for the long term.

Market Recovery on the Horizon

Over the last two years, spikes in inflation saw consumers cut discretionary spending and shy away from annual upgrades to their devices. For Apple, this shift was reflected in revenue declines in each of its product segments. In fiscal 2023, net sales for the iPhone fell by 2% year over year, with Mac revenue plunging 27% and iPad sales sliding 3%.

Apple suffered from declines that affected companies across tech. According to International Data Corporation (IDC), global smartphone shipments decreased 11% in 2022 and continued falling for most of 2023. Other tech markets, like personal computers, saw similar declines during the period.

However, recent data shows a rebound in the industry may have begun. Smartphone shipments rose for the first time in over a year in the fourth quarter of 2023, with IDC reporting a 7% increase. The recovery is projected to continue this year and rise close to 4% in 2024.

Apple’s iPhone segment accounts for more than 50% of its revenue, which made it vulnerable to a market downturn in 2023. However, there may be some light at the end of the tunnel now that tech sales are on the rise and the company is expanding into other sectors.

Persistence and Patience Required

Apple hit nearly $100 billion in free cash flow last year despite declines in its product segment. The figure indicates that Apple has the financial resources to invest heavily in its business and overcome current headwinds.

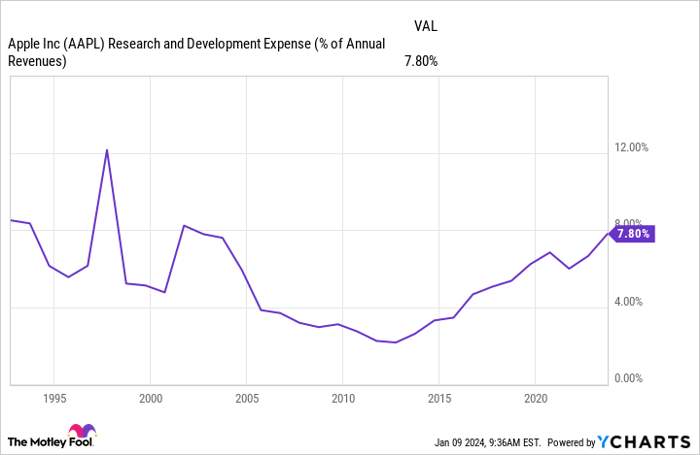

It’s encouraging that Apple increased its research and development spending by close to $4 billion last year, using about 8% of its revenue. The chart below shows that’s the highest percentage spent on research for at least 20 years. In fact, the last time it was higher, Apple was gearing up to release the first iPhone and expand its iPod business.

It’s unclear what Apple’s roadmap looks like for the next decade. However, it almost certainly includes artificial intelligence (AI) and virtual/augmented reality (VR/AR), two rapidly expanding industries.

The AI market on its own is projected to develop at a compound annual growth rate (CAGR) of 37% through 2030, which would see it surpass a value of $1 trillion. Meanwhile, VR is on a similar trajectory, with the sector expanding at a CAGR of 29% over the same period.

Apple CEO Tim Cook has hinted that a significant portion of its research is currently dedicated to AI, with Bloomberg reporting last year that the company had built a large language model similar to OpenAI’s ChatGPT. So far, Apple has used AI to enhance its products, including improvements to Siri and various AI-enabled iPhone and Apple Watch features. However, significant investment could suggest something much bigger is in the works.

Regarding VR/AR, Apple will launch its first headset, the Vision Pro, next month. The new device will debut at $3,499, pricing out many consumers.

However, the headset appears to be a long-term play for Apple to eventually dominate the high-growth sector. Employing a strategy it has often used with past products, the company will likely bring down the cost of the Vision Pro with future iterations while it uses this time to create hype and refine the technology.

Apple’s price-to-earnings ratio of 30 and price-to-sales ratio above 7 suggests its stock is a pricy option. However, comparing those figures to other companies in “Big Tech” shows Apple is actually one of the cheapest stocks besides Alphabet.

It will take time, but an improving consumer market and heavy investment in multiple high-growth areas could spell a lucrative future for Apple. Recent moves see the company expanding its economic moat, which will increase its competitive edge against rivals. As a result, it’s not too late to invest in Apple, with its stock an attractive long-term option.

Should you invest $1,000 in Apple right now?

Before you buy stock in Apple, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Apple wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 8, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Dani Cook has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.