Both the leading automakers, Ford Motor Company F and Stellantis N.V. STLA, have recently announced strategic partnerships to strengthen their respective long-term growth.

On May 18, 2026, Ford Energy signed a five-year agreement with EDF Group to supply up to 20 GWh of battery energy storage systems for U.S. grid-scale projects beginning in 2028.

On June 17, 2026, Stellantis announced a partnership with Wayve and Uber Technologies to accelerate the global deployment of Level 4 autonomous robotaxis by combining vehicle platforms, AI driving technology and ride-hailing capabilities.

While both automakers appear well-positioned for sustained growth, let’s dig deeper into their fundamentals to get a clearer perspective on which company currently holds the stronger competitive advantage.

The Case for Ford Stock

Ford Pro remains a key growth engine, supported by demand for commercial vehicles and expanding software and physical services. In the first quarter of 2026, paid software subscriptions rose 30% year over year to 879,000, reinforcing the shift toward higher recurring revenues. The company expects 2026 Ford Pro EBIT of $6.5-$7.5 billion compared with $6.84 billion in 2025, which keeps the segment central to Ford’s longer-term earnings mix.

Ford’s strategy of emphasizing higher-margin vehicles and trims appears to be working. The strong demand for trucks, large SUVs, off-road trims and hybrids with richer margins is improving profitability. Off-road performance trims, such as Raptor and Tremor, now account for nearly one-quarter of U.S. sales, while Ford also reported improved mix within Explorer, Expedition and F-Series.

Ford maintained lower incentive spending than competitors while still achieving strong transaction prices and retail share gains. This suggests healthier pricing discipline compared with prior industry cycles. The company’s focus on “profit pillars” rather than low-margin volume growth could help sustain earnings even if industry demand moderates over time. For the full year, Ford raised its overall adjusted EBIT guidance to $8.5-$10.5 billion, up from previous guidance of $8-$10 billion.

However, Ford continues to fund modernization, connectivity and new product programs while expanding electrification and services. The company expects 2026 capital expenditures of $9.5-$10.5 billion, up from $8.8 billion in 2025. With additional spending tied to EV development and interim supply-chain costs, cash conversion can remain uneven through the cycle.

The Zacks Consensus Estimate for F’s 2026 EPS implies year-over-year growth of 50.5%. EPS estimates for 2026 and 2027 have improved by 4 cents and 2 cents, respectively, in the past 30 days.

Image Source: Zacks Investment Research

The Case for Stellantis Stock

Industrial costs remain a tailwind for Stellantis, supported by higher production volumes, improved manufacturing efficiency and ongoing product cost optimization initiatives. For 2026, Stellantis projects mid-single-digit revenue growth, a low-single-digit adjusted operating income margin and year-over-year improvement in industrial free cash flow.

On May 21, 2026, Stellantis launched its FaSTLAne 2030 strategy, outlining a €60 billion five-year plan aimed at accelerating growth, improving profitability and enhancing shareholder returns. The company targets revenue growth from €154 billion in 2025 to €190 billion by 2030, a 7% adjusted operating income margin by 2030, positive industrial free cash flow in 2027 rising to €6 billion by 2030, and €6 billion in annualized cost savings by 2028 through its Value Creation Program.

Stellantis also expanded its collaboration with Qualcomm Technologies to integrate Snapdragon Digital Chassis chips with its STLA Brain software platform, strengthening cockpit, connectivity and ADAS capabilities while supporting faster product launches, continuous software upgrades and greater cost efficiency through platform standardization.

Stellantis launched its affordable E-Car project, with production expected to begin in 2028. The fully electric vehicle targets Europe’s shrinking affordable small-car segment and will feature advanced BEV technology developed with partners to enhance affordability and accelerate commercialization.

However, Stellantis continues to face significant raw material cost volatility. Based on prevailing market prices, the net impact after hedging could approach 1% of annual revenues, with raw material costs potentially adding more than €1 billion in expenses during 2026.

The Zacks Consensus Estimate for STLA’s 2026 EPS implies year-over-year growth of 214.6%. EPS estimates for 2026 and 2027 have fallen 4 cents and 12 cents, respectively, in the past 30 days.

Image Source: Zacks Investment Research

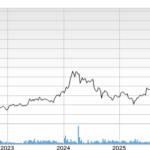

Price Performance of F & STLA

In the last six months, shares of Stellantis have plunged 42.5%, while Ford shares have risen 5.8%. While F has outperformed the Zacks auto sector, Stellantis has underperformed the same.

6-Month Price Performance Comparison

Image Source: Zacks Investment Research

Conclusion

Ford is delivering profitable growth through its high-margin Ford Pro business, favorable vehicle mix, disciplined pricing strategy and improving earnings outlook. Ford is also set to benefit from upward EPS estimate revisions and positive share price momentum.

On the other hand, Stellantis’ long-term growth depends on ambitious strategic initiatives that are still in the early stages. Also, Stellantis faces downward earnings revisions, raw material cost pressures and weaker stock performance.

Although Ford and Stellantis carry a Zacks Rank #3 (Hold) each at present, Ford appears to be the stronger investment choice based on its current execution and earnings visibility. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA’s enormous potential back in 2016. Now, he has keyed in on what could be “the next big thing” in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

Ford Motor Company (F) : Free Stock Analysis Report

Stellantis N.V. (STLA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.