Apple (NASDAQ: AAPL) has witnessed a robust 47% uptick in stock performance in 2023, only to see a 4% slump in 2024. This downturn has set off alarm bells on Wall Street, primarily due to concerns over sluggish iPhone sales, which constitute almost half of Apple’s revenue, and a slowdown in the Chinese market, responsible for a fifth of the company’s sales.

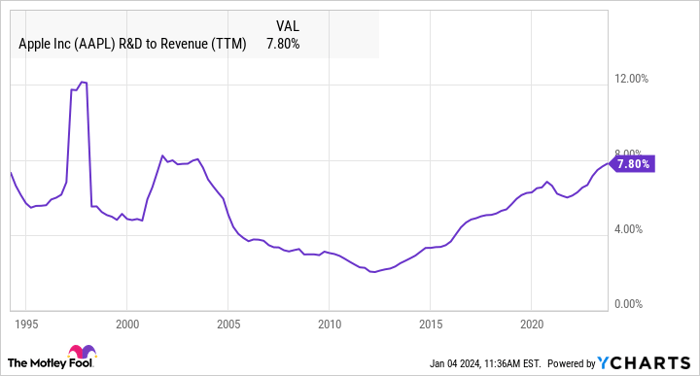

Nevertheless, there’s a brewing storm in Cupertino, California. Apple allocated a staggering 7.8% of its total sales last year to research and development (R&D) expenses, equating to nearly $30 billion. This figure represents the highest proportion of revenue the tech behemoth has spent on R&D in two decades – a time when it was expanding its iPod and music business and conceptualizing the first iPhone.

AAPL R&D to Revenue (TTM) data by YCharts

While Apple’s R&D expenditure has experienced a consistent ascent over the past decade, the absence of a groundbreaking new product since the Apple Watch’s debut in 2015 is conspicuous. With the new Vision Pro headset anticipated this year, the company, however, hasn’t introduced any significant design changes to its existing product lineup for years.

Apple’s Booming Competitive Advantage

During the company’s fiscal fourth-quarter earnings call, CEO Tim Cook alluded to the manifold areas where the surge in R&D spending is being channeled:

“It’s … some things I can’t talk about. It’s Vision Pro. It’s [artificial intelligence] and [machine learning]. It’s the silicon investment that we’re making, the transition with the Mac and other silicon.”

The cryptic “silicon” reference pertains to the shift from Intel processors to in-house chips for Mac and other Apple products.

Apple’s long-standing investment in artificial intelligence (AI) and machine learning, notably in the Siri voice assistant, is a well-documented fact. Cook’s hints, however, suggest a broader strategy at play, potentially heralding a new phase in Apple’s product development roadmap.

Granted, the elephant in the room is Apple’s mammoth size, with an annual revenue of $383 billion. In 2007, when the iPhone revolutionized the industry, Apple was a mere fraction of its current stature. The era of a single device propelling the stock to stratospheric heights is a bygone concept.

Yet, everything Cook alluded to is aimed at fortifying the company’s competitive advantage and cultivating a more lucrative business. This clarifies the continued substantial stake held by Warren Buffett in Apple stock and why investors should ponder retaining their holdings.

Apple’s Investments: A Gift that Keeps on Giving for Shareholders

Although Apple may not have recently unveiled revolutionary products that alter the global landscape, it enjoys a robust profit margin trending back toward record highs. This robust margin was a key driver propelling the stock by 47% in 2023 despite subdued sales.

AAPL Profit Margin data by YCharts

The surge in margins can be directly attributed to the upswing in R&D spending. Cook disclosed that a portion of the R&D increment is earmarked for AI, a technology integral to numerous iPhone features, such as Siri, photo searches, Face ID, and the neural engine enhancing the iPhone’s camera capabilities. These features elevate customer satisfaction and spur spending on services, which yield double the margin from hardware products.

Services, comprising app sales and subscriptions, represent Apple’s fastest-growing segment, expanding by 9% in fiscal 2023. Clearly, the management anticipates sustained services growth over the long haul.

“Our installed base of over 2 billion active devices continues to grow at a nice pace and establishes a solid foundation for the future expansion of the ecosystem,” observed CFO Luca Maestri during the recent earnings call.

Given that services still account for a mere 22% of Apple’s overall sales and are outpacing growth in other revenue categories, their margins and profits are poised for an upward trajectory. Management’s strategic investments center on Apple’s brand and user experience, portending a future of burgeoning profits, dividend advances, and a stock that seems poised to scale new peaks for years to come.

Should you invest $1,000 in Apple right now?

Before you venture into Apple stock, ponder this:

The Motley Fool Stock Advisor analyst team recently pinpointed what they believe are the 10 best stocks set to yield massive returns in the years ahead… and Apple didn’t make the cut. These top selections have the potential to deliver exceptional returns.

Stock Advisor furnishes investors with a user-friendly blueprint for success, offering guidance on portfolio construction, regular analyst updates, and two fresh stock picks per month. The Stock Advisor service has outperformed S&P 500 returns by more than triple since 2002*.

*Stock Advisor returns as of December 18, 2023

John Ballard has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple. The Motley Fool recommends Intel and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short February 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.