Taiwan Semiconductor Manufacturing Company Limited TSM, or TSMC, renowned for crafting the tiniest and most energy-efficient chips, witnessed a recent surge in its shares following a substantial rise in quarterly profits driven by the demand for artificial intelligence (AI).

Diving deeper, TSMC’s upward trajectory is not solely attributed to its 54.2% year-over-year net profit surge to 325.3 New Taiwan dollars ($10.1 billion) in the third quarter, which exceeded analysts’ predictions. The revenues for the July-September quarter soared to $23.5 billion, marking a 36% annual increase.

The Impetus Behind TSMC’s Bullish Run

Our narrative shifts to the core of TSMC’s success story – its quarterly results and promising future prospects. Notably, the sales of the chipmaker’s cutting-edge 3nm chips, deployed in high-performance computers including Apple Inc.’s iPhone, significantly fueled third-quarter revenues. In a forward-looking statement, TSMC’s CFO Wendell Huang projected an upswing in fourth-quarter revenues, citing a surge in demand for these advanced chips. The company’s gross margins peaked at 57.8% in Q3, and projections indicate the margin will remain robust between 57% and 59% in the upcoming quarter, driven by the burgeoning appetite for AI applications.

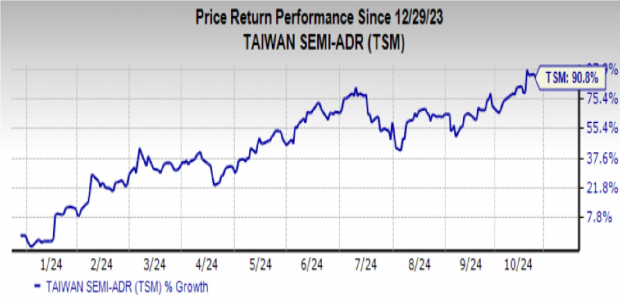

As a consequence of the robust quarterly performance and promising future outlook, TSMC’s shares skyrocketed – having already accumulated a staggering 90.8% gain in value this year.

TSMC’s Positioning for Ascension

TSMC’s ascendancy isn’t a stroke of luck; rather, it’s a result of meticulous planning and strategic positioning in the market. The company holds a dominant position with over 50% of market share among contract manufacturers, illustrating a formidable economic moat. This dominance has fortified TSMC’s relationships with its customers, setting it apart in the competitive landscape. Noteworthy is the fact that NVIDIA Corporation relies entirely on TSMC for its data center components, underscoring TSMC’s operational prowess as evidenced by a 47.5% operating margin in the third quarter.

On the battlefield of competition, TSMC’s immediate rivals face hurdles. Samsung grapples with issues in its memory business, while Intel Corporation is undergoing restructuring endeavors, dismantling capital expenditures.

TSMC’s ability to operate profitably is evident through its net profit margin of 39.6%, surpassing the Semiconductor – Circuit Foundry industry’s 39.1% benchmark for net profit margin. Such formidable margins solidify TSMC’s stance in a league of its own.

The relentless demand for AI serves as a tailwind propelling TSMC’s growth trajectory. The company’s proactive steps, including the establishment of chip-manufacturing plants in Arizona, Europe, and Japan to meet the surging demand for advanced chips, further cement its position as an industry leader in the AI space.

Seizing the Opportunity

Given the promising road ahead, investing in the beacon of the semiconductor industry, TSMC, seems judicious. Analysts peg the short-term target price for TSM stock at $216.14, indicating a potential 7% upside from its recent closing price of $201.95. The highest short-term price target stands at $250, signaling a substantial 23.8% potential increase.

Moreover, the Zacks Consensus Estimate projects a 14.3% annual increase in TSMC’s earnings per share, lining the company for continued success, hence meriting a Zacks Rank #2 (Buy).