Investing in growth stocks can be like adding fuel to your financial engine. Unlike traditional value stocks, these equities often pack a dynamism that can fire up your portfolio’s earnings potential.

One key advantage of growth stocks is their potential to unleash untapped possibilities. Over time, these stocks may magnify returns, offering a path for long-term wealth accumulation through compounding.

Many growth stocks reside in sectors characterized by innovation and disruptive technologies. Investing in these companies exposes you to industries that are not simply shaping the future, but also promising significant returns over time.

In this article, we’ll explore two unique growth stocks from different sectors, offering investors the opportunity to diversify their holdings.

Meet our first contender, the semiconductor company Advanced Micro Devices (AMD). While Nvidia reigns as the sovereign in the chip industry, AMD has steadily solidified its position in recent years. The journey of AMD’s stock price is nothing short of spectacular. Over the last decade, it has increased an astonishing

4,215%

.

Our second pick, the e-commerce company Etsy (ETSY), gained widespread recognition during the pandemic. Its evolution from a niche marketplace to a global e-commerce juggernaut, even in the post-pandemic era, showcases remarkable resilience.

Let’s delve into why these two stocks are red hot choices for investors in 2024 and beyond.

Advanced Micro Devices Stock Overview

With a market cap of $236.8 billion, AMD is disrupting the dominance of its competitors and carving out a significant niche in the semiconductor space. Renowned for its innovative products and strategic advancements, AMD’s trajectory has been impressive with promising prospects.

In the past year, its stock surged by an astonishing

127%

, far outpacing the tech-heavy Nasdaq Composite’s gain of 43.4%.

AMD’s fundamentals thrived in 2023, propelled by the artificial intelligence (AI) boom. Following a slight slump in its data center business last year, the segment is gradually rebounding, maintaining a flat revenue of

$1.6 billion

year-over-year in the third quarter. Sequentially, the metric surged by 21% owing to the rapid adoption of AMD’s 4th Gen EPYC CPUs by customers.

Total revenue stood at $5.8 billion, marking a 4% annual increase. Diluted earnings per share (EPS) also leaped by 4% to $0.70 during the quarter, surpassing the consensus estimate by $0.02 per share.

AMD’s growth story extends beyond the consumer and data center segments. The company has made significant strides in other markets, including gaming consoles.

According to CEO Lisa Su, AI represents a “multibillion-dollar growth opportunity for AMD across cloud, edge, and an increasingly diverse number of intelligent endpoints.”

In a bid to integrate open AI software into its hardware, AMD completed strategic acquisitions in 2023 – specifically, the purchases of open-source AI software expert Nod.ai and AI software leader Mipsology.

In the aftermath of Q3, the company unveiled several significant AI-powered high-end processors, including the Ryzen Threadripper PRO 7000 WX-Series processors, Ryzen Threadripper 7000 Series processors, Ryzen 7045HX3D Series mobile processors, and the Ryzen 5 5600X3D processor tailored for gaming.

Looking forward, as AI gains momentum, AMD’s growth prospects appear robust over the coming years. The sustained demand for high-performance graphic processors across several sectors bodes well for the company.

Management anticipates

fourth-quarter revenue

to hover around $6.1 billion (plus or minus $300 million), in line with the consensus estimate of $6.14 billion. Furthermore, analysts forecast a 17% year-on-year revenue surge by 2024.

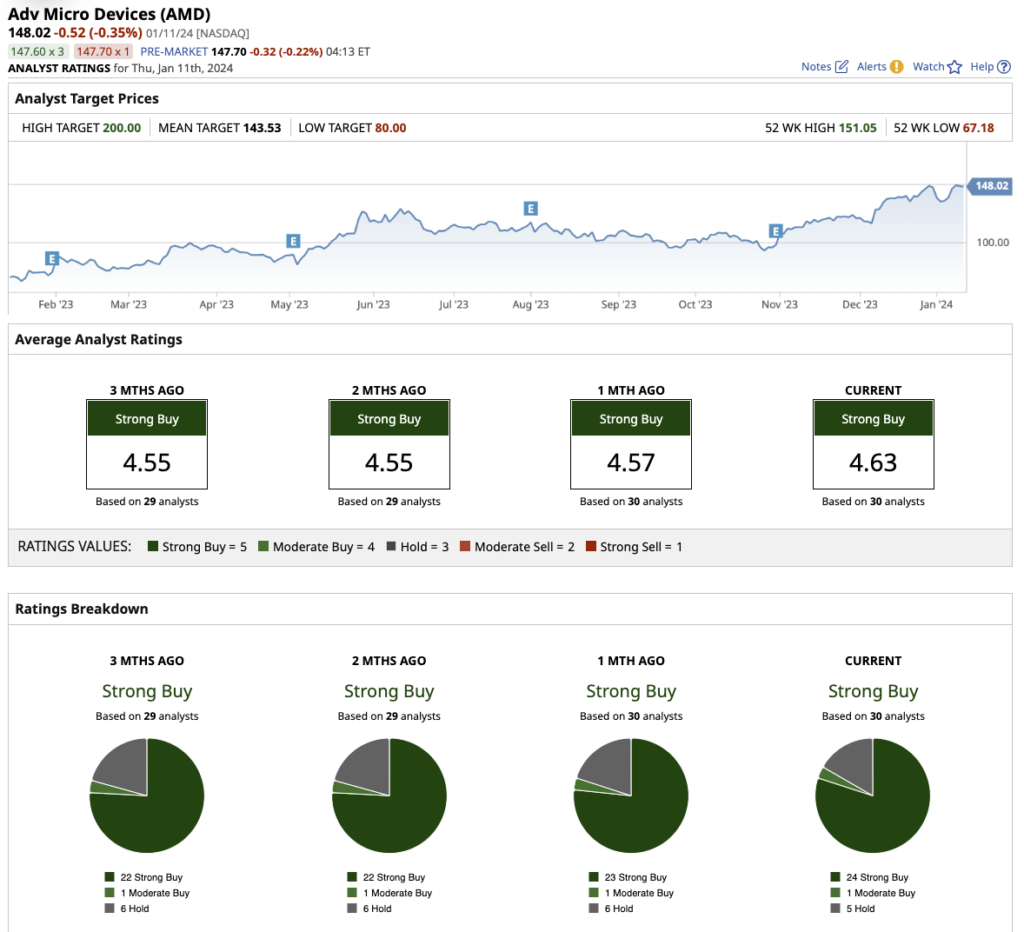

What Analysts Are Saying About AMD

With a promising outlook for chip stocks, analysts at Stifel, KeyBanc, Bernstein, Mizuho, Truist, and several others have raised the target price for AMD stock this month.

On the whole, Wall Street has bestowed a “strong buy” rating on AMD. Out of the 30 analysts covering the stock, 24 rate it a “strong buy,” with one “moderate buy” rating, and five “hold” ratings.

AMD has already surpassed its average target price of

The Evolving Landscape: Etsy’s Financial Outlook

Investors in the ever-fluctuating world of e-commerce have witnessed a peculiar ascent: the unparalleled growth and transformation of Etsy, an online marketplace that has amalgamated creators, artisans, and buyers into a thriving ecosystem. Since its inception in 2005, Etsy has metamorphosed from a niche platform exclusively catering to handmade and vintage items to a global marketplace catering to an expansive community of sellers and buyers, carving out a distinctive niche in the industry.

Even amidst the tumultuous winds of the COVID-19 pandemic that ushered in unprecedented challenges for consumer discretionary spending, Etsy absconded the mire and showcased robust growth, defying conventional economic wisdom.

The Company’s Financial Performance

In its most recent third quarter, Etsy recorded an impressive addition of 6 million new buyers to its platform. Notably, the company’s consolidated gross merchandise sales (GMS), a pivotal metric measuring the total value of goods sold on the platform, bolstered by 1.2% to $3.0 billion. Consequently, this led to a formidable 7% surge in revenue, amassing to $636.6 million, compared to the previous year. Management attributed this revenue growth to the stellar performance of “Etsy Ads, payments revenue, and transaction fee revenue from Offsite Ads.”

Etsy’s meteoric rise is further underscored by its attainment of a net income of $87.9 million, a staggering contrast to the $963 million loss incurred in the year-ago quarter. In a bid to foster further financial buoyancy, Etsy implemented a seller transaction fee hike from 5% to 6.5% in April 2022. Contrary to conventional reasoning, the fee hike did not deter sellers; the platform experienced a 19% uptick in active sellers, reaching 8.8 million during the third quarter.

Looking forward, Etsy’s growth trajectory seems to be enveloped in optimism, buoyed by its distinctive business model and a proclivity to adapt to prevailing market trends. The company remains favorably positioned to capitalize on the burgeoning prevalence of online shopping, its unwavering commitment to community building, and its adeptness in aligning with evolving consumer aspirations for unique and sustainable products—attributes that give it an edge in the e-commerce landscape.

Analyst Projections and Investor Sentiment

Amid the juxtaposition of fervent optimism and tempered caution, Wall Street echoes a somber note, expressing skepticism about Etsy’s potential to weather macroeconomic headwinds and report dramatic growth. However, a closer look reveals a contrasting narrative as Etsy is envisaged to embark on a steady growth trajectory, with projections signaling a 5.4% surge in revenue and a 3.8% rise in earnings for 2024.

Strikingly, Etsy currently trades at 15 times the forward 2024 earnings, a valiant shift from its historical five-year average price-to-earnings ratio of 55, ushering in an avant-garde era for the company and investors alike.

Analyst Consensus

The consensus among analysts predicates Etsy as a “moderate buy,” with 27 industry experts lending their perspectives. Out of this cohort, 10 analysts bestow Etsy with a “strong buy” rating, while two advocate a “moderate buy.” A further 13 analysts opine that it is prudent to “hold” the stock. However, amidst these voices of optimism, lurk the contrarian views of one analyst who recommends a “moderate sell,” and another who advocates a “strong sell.”

Concurrently, the mean target price for Etsy stock stands at $85.58, denoting a 20.4% potential upside from current levels. Diverging from the mean, the Street-high price target of $170 projects an audacious 139% anticipated upside, emanating a spirited optimism fermenting within the finance community.