The Contrarian Case for New Gold Mining Stock

In a marketplace where gold prices are scaling lofty summits, the allure of gold mining stocks has dimmed considerably. Historically, the fate of gold mining equities has mirrored the trajectory of the precious metal they extract. Yet, in an unusual turn of events, concerns about inflation and rising interest rates have cast a shadow on these capital-intensive mining enterprises.

This very lag in performance presents an opportunity to secure quality mining stocks that are currently trading at a discount, promising substantial returns when market sentiment shifts. Amidst this climate, one such under-the-radar prospect is New Gold (NGD), presenting an intriguing proposition for investors looking to capitalize on the rebound potential in the gold mining sector.

Peering into New Gold’s Galaxy

A market capitalization of $1.3 billion adorns New Gold, a Canadian intermediate mining firm. Positioned between junior and senior gold miners, intermediate players like New Gold possess a blend of size and maturity that distinguishes them in the industry landscape. Anchored in Canada, New Gold operates two foundational assets – the Rainy River gold mine and the New Afton copper-gold mine.

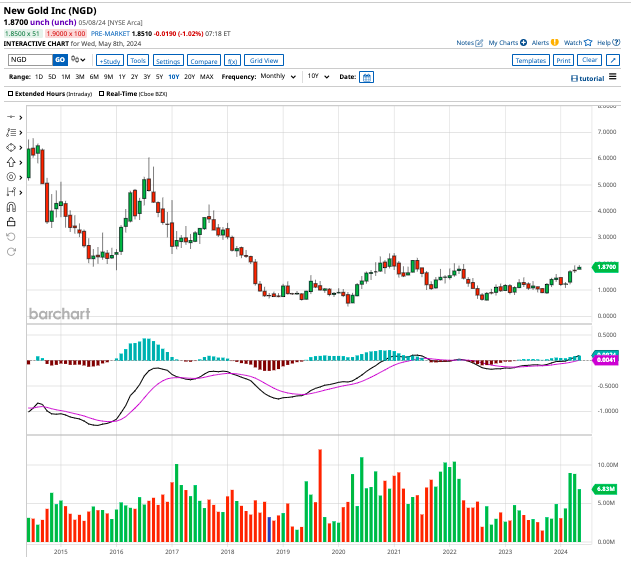

Bolstered by the recent bull run in gold prices, NGD stock has surged 34% year-to-date, marking an impressive 127% spike from its 52-week low recorded in October. However, the stock’s long-term voyage reveals a stark narrative – having relinquished over 60% of its market value in the last decade.

Against this backdrop, the pivotal question looms – does New Gold hold the promise of a golden goose in 2024? Let’s delve into the numbers to unearth the hidden truths.

Unveiling New Gold’s Performance in Q1 of 2024

During the March quarter, New Gold unfurled its production prowess, boasting 70,900 ounces of gold and 13.3 million pounds of copper. Notably, the Rainy River mine contributed 52,700 ounces of gold, while New Afton chipped in with an additional 18,200 ounces – aligning closely with management’s projections. This explicitly signifies an 11% uptick in gold output and a 29% surge in copper production compared to the corresponding period last year.

With all-in sustaining costs (AISC) amounting to $1,396 per ounce, New Gold anticipates a downtrend in production costs as 2024 unfolds.

Despite notching revenues of $192 million in Q1, a dip from the prior-year period owing to reduced sales volumes, New Gold’s operational cash flow stood at $73 million, translating to $0.11 per share – delineating a robust margin of nearly 40%. Concurrently, adjusted earnings slipped to $13 million, or $0.02 per share, juxtaposed with $18 million in the analogous quarter.

Capital outlays of $61 million steered by New Gold in Q1 included a significant $35 million earmarked for growth ventures, while the remainder was allocated to sustaining capital necessities. Noteworthy among these were capitalized waste, components, and tailings management and construction expenses.

The conclusion of Q1 witnessed New Gold boasting a cash reservoir of $157 million coupled with total liquidity amounting to $530 million, lending the company a nimble buffer to navigate through a realm fraught with macroeconomic uncertainties. Anchored by a robust financial foundation, firmly underscored by its strategic investments in organic growth, New Gold stands poised to harness the buoyancy of the heightened metal price milieu, eventually translating into robust free cash flows.

Forecasting the Trajectory of New Gold’s Skyline

Of the nine keen-eyed analysts tracking New Gold’s trajectory, two espouse a “strong buy” sentiment, while two favor a “moderate buy,” paralleled by three “hold” ratings. At the opposing end of the spectrum, one analyst advocates a “moderate sell,” while another casts a “strong sell” vote.

With the mean 12-month target price for NGD stock pegged at $1.92 – languishing below the current trading price – the slimmest ray of optimism manifests in the form of a Street-high target of $2.36, marking a premium of nearly 20% vis-a-vis prevailing levels.

Prognostications regarding New Gold’s financial performance unveil an anticipatory uptrend. Forecasts chart an upward trajectory in sales, foreseeing a 16% surge to $912 million in 2024, further elevating to $1.04 billion in 2025. The journey of adjusted earnings is slated to commence from $0.07 per share in 2023, gradually swelling to $0.12 per share in 2024 and culminating in $0.23 in 2025.

With New Gold stock trading at a modest 15.6 times forward earnings – despite registering a 5% uptick in today’s trading – the allure of this undervalued gem beckons, presenting an enticing proposition for shrewd investors discerning long-term value amidst the market tumult.