The rapid advancements in artificial intelligence (AI) have significantly impacted various industries, making AI stocks appealing to investors seeking growth opportunities. Among the many contenders in this space, tech giant Microsoft (MSFT) has emerged as a key player with its robust AI capabilities. The company had an impressive start to fiscal 2024, with outstanding growth across all its segments.

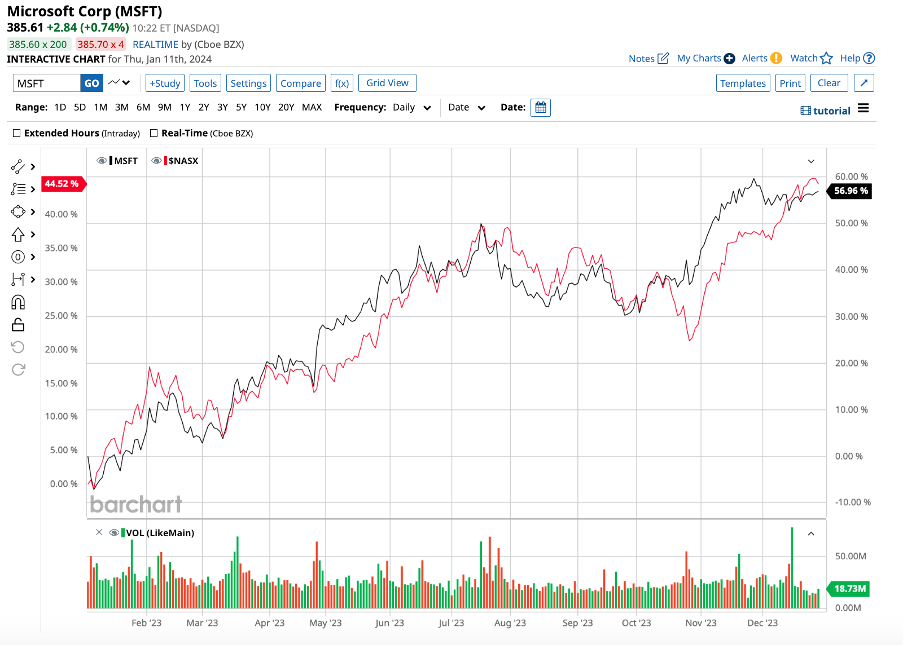

Last year, the stock soared 57%, outperforming the tech-heavy Nasdaq Composite ($NASX), which rose 44.5%.

Of course, Microsoft has run a very successful business even before the AI rush took over. Its financial stability and consistent revenue growth made it an appealing investment over the years, driving its stock to returns of 926% over the last 10 years.

Nonetheless, I believe there is much more AI potential to be unlocked, and the stock could reach its Street-high target price of $600 this year.

Unleashing the Power of AI at Microsoft

Founded in 1975, Microsoft has blossomed into a global tech titan that provides software, hardware, cloud computing, and other services.

Microsoft’s revenue has increased significantly over the last five years as a result of its diverse operations. Notably, revenue has climbed from $126 billion in fiscal 2019 to $212 billion in fiscal 2023, while earnings per share (EPS) have gone up from $5.06 to $9.68 during the same time.

Microsoft’s cloud computing platform, Azure, provides an extensive set of AI services. Azure’s scalable and flexible environment allows developers and businesses to seamlessly integrate AI solutions, ranging from machine learning to natural language processing. The widespread adoption of Azure by enterprises has solidified Microsoft’s standing in the AI market.

Furthermore, with a 22% market share, Microsoft’s Azure is ranked second in the cloud computing market, trailing only Amazon’s (AMZN) AWS (Amazon Web Services).

The success of cloud is driving Microsoft’s growth, as seen in its most recent first quarter of fiscal 2024. Intelligent Cloud segment revenue came in at $24.3 billion, an increase of 19% year-over-year, accounting for the majority of Microsoft’s total revenue of $56.5 billion, which grew 13% from the prior-year quarter. Operating income for the segment also surged 31% to $2.8 billion.

Notably, Azure revenue increased 29% year-on-year in the first quarter. CEO Satya Nadella highlighted that “more than 18,000 organizations now use Azure OpenAI Service.”

Microsoft has successfully incorporated AI capabilities into its existing product ecosystem, which includes Windows, Office 365, and Dynamics 365. All of its segments’ revenue grew in the first quarter. Management anticipates Productivity and Business Processes segment revenue to be in the 11% to 12% range in Q2.

While the slow recovery in the personal computing market has been a drag on sales, management expects the Activision Blizzard acquisition deal (closed in October) to drive the segment’s revenue in the $16.5 to $16.9 billion range for Q2. This would represent a growth of 16% to 19% in the Personal Computing segment over the year-ago quarter.

The AI Growth Story Is Just Getting Started

The company’s diverse revenue streams, which include cloud services and now AI-related products, help to strengthen its overall position in this competitive market.

Management believes Azure’s revenue will jump by 26% to 27% in constant currency terms, causing the Intelligent Segment revenue to fall in the $25.1 billion to $25.4 billion range in Q2.

For Q2 fiscal 2024, analysts expect Microsoft to report a 16% increase in revenue to $61.04 billion and a 19% increase in earnings to $2.76 per share. Furthermore, analysts predict revenue and earnings will increase by 14% and 15%, respectively, for the full fiscal year 2024.

Microsoft is set to release its Q2 earnings on Jan. 31, and we will learn more about Microsoft’s plan for fiscal 2024 then.

Microsoft trades at 34 times forward fiscal 2024 earnings, compared to its historical five-year average price-to-earnings ratio of 29. While it seems expensive, Microsoft’s long-term AI prospects might make it worth paying the premium.

Expert Opinion on MSFT

Recently, MarketWatch quoted Wedbush analyst Daniel Ives as saying, “The stock has yet to price in the next wave of cloud and AI expansion due to Microsoft’s strong competitive cloud edge.” Impressed with Microsoft’s AI products, Ives increased the target price on MSFT

Microsoft’s AI Pioneering: A Look into Copilot

It is no secret that Microsoft has been a trailblazer in the world of artificial intelligence (AI). With the recent announcement of its Copilot AI system, the tech giant has stepped further into the limelight, garnering attention from investors and analysts alike. Let’s take a deeper dive into the implications of this groundbreaking technology and its potential impact on Microsoft’s future.

The Rise of Copilot

In a move that has captivated the market, Microsoft unveiled its Copilot AI system, which has been hailed as a game-changer in the AI space. Analyst Daniel Ives of Wedbush Securities voiced his bullish outlook, setting a price target of $450 with a “strong buy” rating for Microsoft. Ives went so far as to predict that Copilot will generate $25 billion in revenue for Microsoft by fiscal year 2025.

Impressive Milestones

During the Q1 earnings call, Microsoft’s CEO revealed that the company has reached the milestone of 1 million paid Copilot users, with over 37,000 organizations subscribing to Copilot for Business. These figures demonstrate the rapid adoption and widespread appeal of Microsoft’s AI technology in the market.

Competitive Landscape

Despite facing formidable competition in the realms of cloud services, machine learning, and natural language processing, Microsoft stands toe-to-toe with tech titans such as Amazon and Alphabet (GOOGL). Ives remains sanguine about Microsoft’s competitive advantage in the cloud, emphasizing its potential to outperform rivals.

I share Ives’ optimism and believe that Microsoft is well-positioned to surpass Amazon and Google in the realm of cloud computing.

Market Sentiment

Wall Street’s sentiment towards Microsoft is overwhelmingly bullish, with an overall “strong buy” rating. Out of 37 analysts covering the stock, 31 rate it as a “strong buy,” underlining the widespread confidence in Microsoft’s future. The stock’s average target price is noted at $408.34, signifying a 5.1% upside potential from current levels, with a high target price of $600 suggesting a substantial 54% potential for growth.

The Bottom Line

Microsoft’s foray into the AI space with Copilot signifies its commitment to innovation and market leadership. While the competitive landscape is intense, Microsoft’s robust AI platform, strategic acquisitions, integrated solutions, and legacy products position it as a formidable player in the market.

My optimism towards Microsoft’s ability to reach its high target price of $600 is unwavering, making it my top AI stock pick for 2024.